[12/52] The Physical Imperative: Critical Minerals, Supply Chain Vulnerabilities, and Friend-Shoring

A deep dive trend oriented financial research article covering Oil, Critical Minerals, Supply Vulnerabilities, Mining, and Reshoring of our Industrial Base: This research took me (@Donversationz) a long time to study, learn, and edit. If you find it educational, please consider helping us spread the message on X, in DMs, and with friends.

The Digital-Only Reign is Over as we Shift Back to a Physical Economy ran by Tradespeople, Mining Companies, and Rare Earth Elements

The prevailing economic narrative of the 21st century suggested a steady dematerialization of the global economy. As capital flowed into cloud computing, artificial intelligence, and global telecommunications, a dangerous illusion took hold: that the digital realm had somehow decoupled from the physical realm. By 2026, this illusion has been systematically dismantled by geopolitical realities. The digital domain is, and always has been, entirely tethered to the physical substrate.

You’re able to read this digitally on the internet because of physical fiber-optic cables drawn from ultra-pure silica glass via chemical vapor deposition and high temperature extrusion transmitting data as light pulses across continents and oceans, supported by silicon semiconductors refined through zone melting and doped with elements like phosphorus or boron for transistor functionality in your device, all powered by electricity conducted through copper or aluminum wires laid by steel-heavy trenching machines, and augmented by constellations of satellites orbiting at 550 kilometers altitude, launched atop multi-stage rockets like the Falcon 9, which propel payloads using combustion of refined kerosene and liquid oxygen researched by Robert Goddard in the 1920’s.

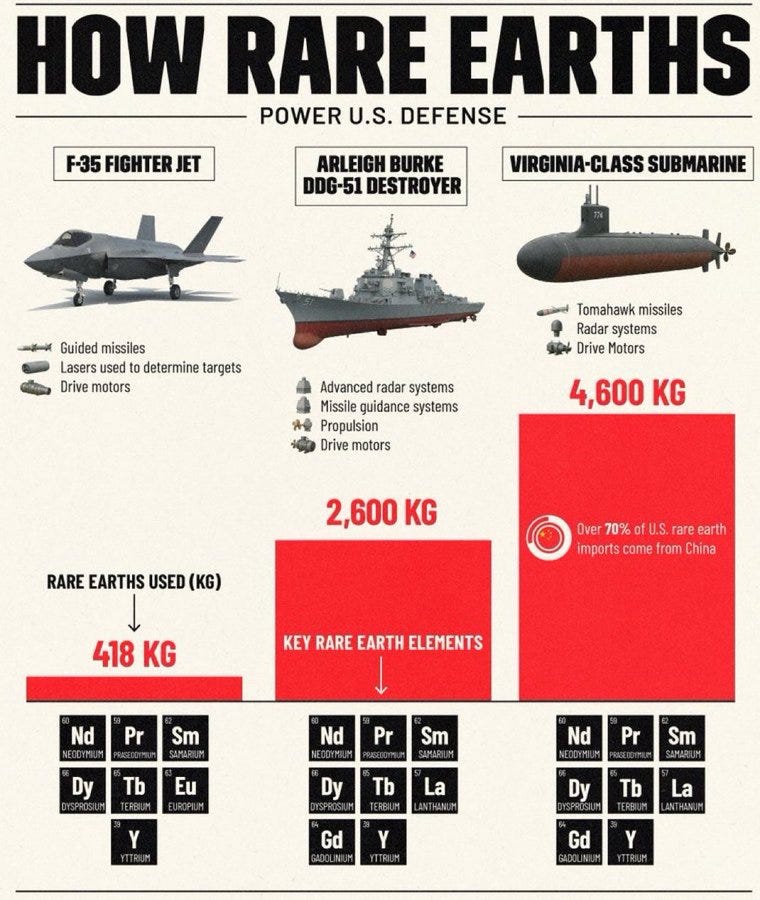

The most important materials in the context of technology, national security, defense (including radars, satellites, missiles, night vision, ammunition, and advanced electronics), aren’t just guesses. They’re backed by official U.S. government assessments like the USGS’s final 2025 List of Critical Minerals (60 minerals total, deemed essential with vulnerable supply chains) and targeted lists from DOD, NATO allies, and policy analyses focusing on defense and technology priorities.

For example, Antimony is a chemical element extracted from complicated combinations of these minerals. Without antimony, we’d have no hardened lead bullets for ammunition, no gallium antimonide (GaSb) substrates enabling high-performance infrared detectors in night vision goggles and thermal imaging systems, no critical antimony based semiconductors powering infrared sensors for missile guidance and targeting, and severely compromised radar and satellite capabilities reliant on advanced electronics where antimony compounds enhance diodes, precision optics, and communication hardware that trace back to refined physical materials extracted from the earth and processed via high-temperature metallurgy and chemical vapor deposition.

This single metalloid, designated a critical mineral for U.S. national security, underpins everything from necessary armor-piercing rounds (where it alloys with lead for durability and penetration) to the type-II superlattice structures in InAs/GaSb detectors that provide superior sensitivity for detecting heat signatures in low-light or obscured environments, directly supporting defense radars, reconnaissance satellites, and battlefield dominance. And to be clear.. that is just ONE critical material, there are 50+ if not 100’s. And they are all critical. All day every day the world is going through this process of extracting and crafting the products we take for granted. But after this post, you will appreciate the significance.

It’s become more important than ever in 2026 to manage this entire process on shore, locally, with minimal supply chain risks. And so today we dive into the most important raw materials, their resulting impact on production, and which USA companies are leading the charge.

The vulnerability of the global supply chain for these critical minerals has reached an unavoidable inflection point. Frenemy nations have successfully weaponized their monopolies on the extraction and refinement of these materials, instituting sweeping export bans on elements critical to the defense industrial base. In response, the United States has initiated a paradigm shifting industrial policy. Moving away from the “margin optimized globalization” theme of the late twentieth century, and transiting into a direct equity partner and market-maker for domestic mining, refining, and manufacturing operations. Hate it or love it, it is happening. My job is not to judge, my job is to understand and profit.

My exhaustive research details the technical, geopolitical, and economic state of the physical economy in 2026 (and its unbreakable ties to the digital). It analyzes the newly updated United States Geological Survey Critical Minerals List, dives deeply into the physical and chemical properties that make these materials irreplaceable in technology, defense applications, examines the corporate entities leading the reshoring effort, and evaluates the skilled infrastructure workforce required to build this domestic industrial base. The ultimate reality is stark: our technology and military are entirely dependent on the successful extraction, refinement, and manufacturing of raw physical materials from remote domestic and allied supply chains. And as always, I’m optimistic. I’m optimistic that the USA has another 250+ years of dominance, and I look forward to my grandkids’ grandkids’ grandkids celebrating the 500th anniversary of the USA; the most self sustained country in the world.

The Macroeconomic Shift: From Margin Optimization to Supply Chain Resilience

For four decades, the global economy operated almost exclusively on the principle of comparative advantage, optimizing supply chains for maximum financial margin. The extraction of raw ore and the heavy industrial refinement of pure elements were systematically offshored to jurisdictions with lower labor costs, weaker currencies, heavily subsidized energy, and less stringent environmental regulations. The natural outcome of this economic optimization was that adversarial nations accumulated dominant positions across the entire value chain of modern technology, and in return they purchased our debt. By controlling the processing capacity for rare earth elements, gallium, germanium, and antimony, foreign monopolies positioned themselves at the narrowest choke points of the global economy. None of this was made clear until Trump pointed it out, and I believe he correctly identified the underlying risk. You can debate his mechanisms, but it is hard to debate the underlying risk.

The cascading supply chain failures of recent years, coupled with rising geopolitical tensions, demonstrated that margin optimized supply chains possess zero resilience to systemic shocks. In the context of COVID, a supply chain disruption caused extreme price hikes and delayed product launches. But now in the context of national security, the inability to source antimony for armor-piercing munitions, or gallium for missile defense radars, represents a catastrophic vulnerability. As Warren Buffett teaches, the first thing he looks for when analyzing the long term durability of a company is to ensure there is a low probability of a long-tail catastrophic event which crashes the company. So a disruption in USA Defense supply chains halts the production of military assets, rendering trillion dollar military platforms completely inert, and also opening up global allies to vulnerabilities.

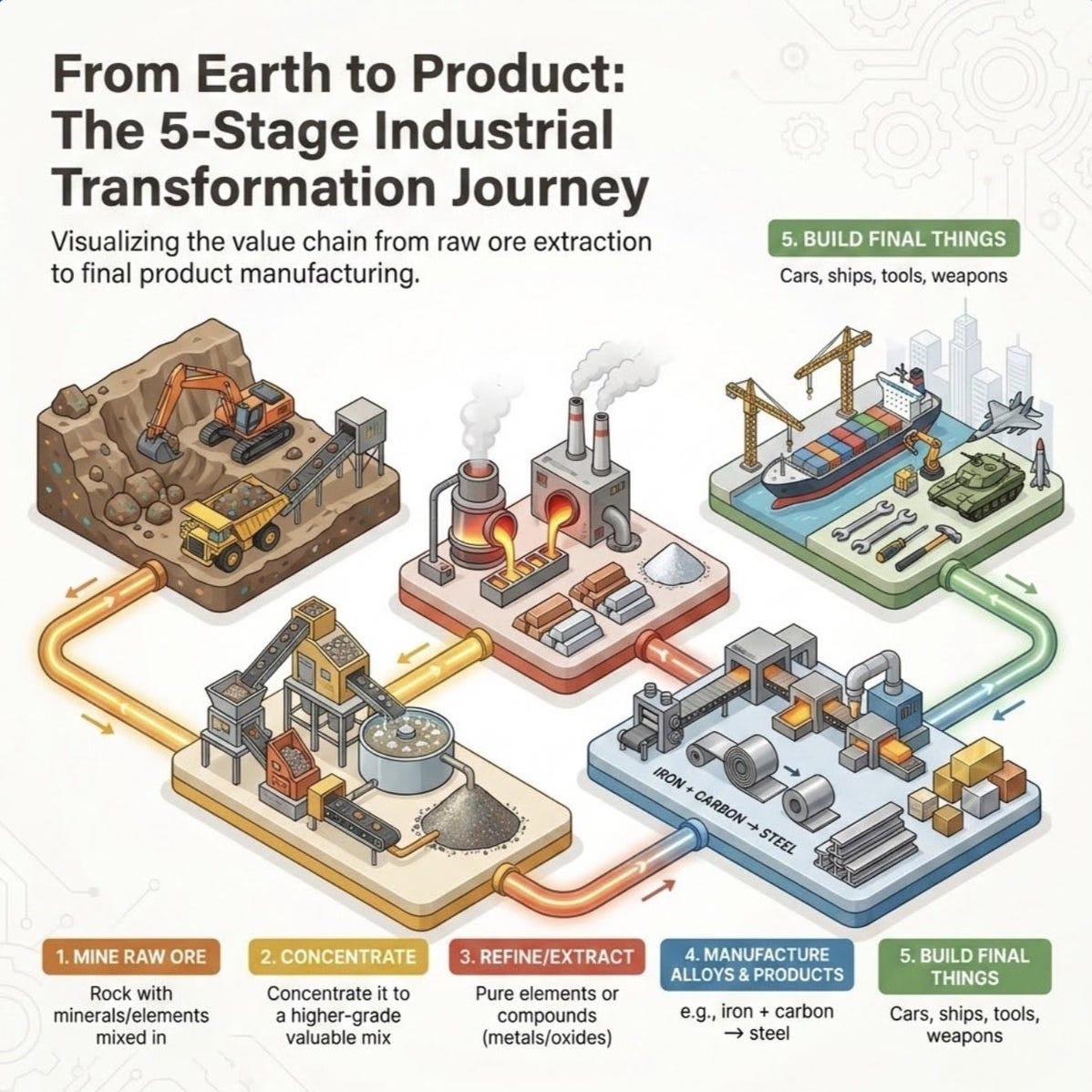

By 2026, the economic calculus of the United States has fundamentally shifted from a pure free-market approach to a hybrid state-capitalist model concerning critical infrastructure. The federal government, utilizing mechanisms like the Defense Production Act, the Department of Energy Loan Programs Office, the Office of Strategic Capital, and the Export-Import Bank of the United States, is actively subsidizing, financing, and taking direct equity stakes in domestic critical mineral projects. This transition acknowledges that national security shall dictate capital allocation alongside traditional market forces, ensuring that the entire process from mining raw ore, concentrating it to a higher-grade mix, extracting pure elements via high-temperature metallurgy, manufacturing specialized alloys, and building final defense products can be executed onshore or within tightly allied networks.

The 2025 Critical Minerals List and Geopolitical Weaponization

The foundational document driving this industrial pivot is the finalized 2025 List of Critical Minerals, published by the Department of the Interior through the United States Geological Survey. The 2025 list outlines 60 minerals deemed vital to the domestic economy and national security, all of which face severe potential risks from geopolitics.

The 2025 update marked a significant expansion from previous iterations, utilizing updated data-driven methods to assess how supply disruptions could paralyze the nation. Based on new data, public feedback, and urgent interagency recommendations from the Departments of Agriculture, Energy, and Defense, ~10 new minerals were added to the critical list.

Expansion of the Strategic Baseline: Newly Added Mineral Justification and Primary Defense/Economic Applications

The Department of Energy was particularly vocal during the interagency review period regarding the addition of metallurgical coal and uranium. The underlying logic is that advanced technologies are irrelevant without uninterrupted baseload power and the physical steel required to build heavy defense platforms.

The Weaponization of the Supply Chain

The urgency surrounding the list is driven by the overt weaponization of critical minerals. As global trade fractured, the Ministry of Commerce of the People’s Republic of China implemented strict export controls and outright bans on a specific cohort of mineral commodities including gallium, germanium, antimony, tungsten, and tellurium.

Because a single nation produces the vast majority of the world’s refined gallium and controls the majority of the antimony and tungsten markets, these export bans were precisely targeted to cripple external industrial bases. This maneuvering has compelled the United States and Allies to rapidly initiate friend-shoring initiatives and fund domestic “mine-to-X” supply chains.

Mind Blowing Deep Dive: The Physics and Engineering of Defense Minerals

To truly comprehend the strategic gravity of the current friend-shoring effort, one must delve into the physical, chemical, and atomic properties of these materials. These elements are not chosen arbitrarily by defense contractors; they possess unique atomic structures that make them fundamentally irreplaceable in high-stress, high-frequency, and high-temperature military use cases.

Gallium and the Evolution of the Electromagnetic Spectrum

Gallium is a soft, silvery metal that has become the linchpin of modern electronic warfare and radar detection. Historically, military radar systems relied on mechanically steered arrays of large physical dishes that physically rotated to scan the horizon. Modern stealth fighters, such as the F-35 Lightning II, and advanced naval surface combatants utilize Active Electronically Scanned Array radars. These modern radar systems consist of hundreds or thousands of individual solid-state modules to transmit and receive. Instead of moving a physical dish, the radar shifts the phase of the radio waves emitted by these distinct modules, allowing the system to steer the beam electronically at instantaneous speeds, track multiple hypersonic targets simultaneously, and perform highly classified electronic attack and electronic support measures.

The foundational semiconductor material for earlier generations of these transmit and receive modules was Gallium Arsenide. However, the defense industry is undergoing a systemic transition to Gallium Nitride.

Gallium Nitride is a wide-bandgap semiconductor. The physical properties of its crystalline lattice allow it to withstand substantially higher electric fields than Gallium Arsenide or Silicon before experiencing electrical breakdown. This atomic resilience translates directly into profound advantages on the tactical battlefield. Mainly:

Power Density and Efficiency: Practical implementations of Gallium Nitride technology achieve power-added efficiencies of up to 65%, compared to merely 25-40% for Gallium Arsenide systems. This allows radar modules to transmit significantly more radio frequency power in a much smaller physical form factors.

Thermal Handling Capabilities: Radar transmission generates immense heat. Gallium Nitride systems can operate at substantially higher junction temperatures while maintaining stable electronic performance. This drastically reduces the need for heavy, complex liquid cooling systems within the constrained airframes of fighter jets, enabling more compact system designs and contributing to much longer component lifespans under stress.

High-Frequency Performance: Gallium Nitride also maintains its efficiency advantage at high frequencies, making it fundamentally superior for targeting radars and the sophisticated seekers built into the nose cones of precision missiles.

Advanced radar systems, such as the airborne arrays developed for the F-35 and the naval radars deployed across modernized fleets, are entirely dependent on a continuous, secure supply of highly refined gallium. Enabling Military superiority in the electromagnetic spectrum, rendering stealth aircraft impervious and strengthening missile defense shields.

Antimony: Kinetic Lethality and Infrared Detection

Antimony is an ultra-critical metalloid designated as a national security priority because it serves irreplaceable, dual-purpose roles in both kinetic warfare and advanced optical sensors.

In its kinetic applications, antimony is alloyed to manufacture hardened bullets and sophisticated munitions. Pure lead/led is far too soft to reliably penetrate modern ballistic materials or hardened vehicle armor. The addition of antimony chemically alters the crystalline structure of the lead, increasing its strength, and durability, without sacrificing the necessary mass required for deep kinetic penetration.

However, antimony’s most advanced and technologically complex application is in the fabrication of mid-wavelength infrared and long-wavelength infrared detectors. Historically, high performance thermal imaging systems and heat seeking missile guidance sensors relied on Mercury Cadmium Telluride. While effective in certain environments, Mercury Cadmium Telluride is notoriously difficult to manufacture uniformly over large focal plane arrays, suffers from long-term stability issues, and requires extreme, bulky cryogenic cooling systems to minimize electronic noise.

The modern defense solution relies on Antimony-based Type-II Superlattices, specifically utilizing alternating nanometer-thick layers of Indium Arsenide and Gallium Antimonide. A superlattice is an artificial crystal structure created by depositing these alternating layers via a highly complex process known as molecular beam epitaxy, usually occurring in multi-wafer high-vacuum reactors.

The Indium Arsenide and Gallium Antimonide superlattice operates on a specific “broken-gap” type-II band alignment. This quantum mechanical property allows defense engineers to artificially tune the effective energy bandgap of the sensor material simply by changing the microscopic thickness of the alternating layers. This means the sensor can be tailored perfectly to detect specific thermal wavelengths, ranging from three micrometers up to over twelve micrometers. Furthermore, the most advanced “M-structure” superlattices introduce an additional layer of Aluminum Antimonide. This layer acts as an energetic barrier for electrons in the conduction band and a double quantum well for holes in the valence band, significantly reducing the electrical noise that obscures thermal images.

The practical result is a thermal sensor that offers superior sensitivity for detecting faint heat signatures in low-light, obscured, or extreme battlefield environments. These superlattices provide unmatched fidelity for reconnaissance satellites surveying the globe, infantry night vision goggles, and the infrared seekers on advanced missiles. The recent foreign export bans on antimony are explicitly designed to throttle the production of these exact defense systems.

Rare Earth Elements: The Physics of Permanent Magnets

The term “Rare Earth Elements” refers to a specific group of 17 chemically similar elements on the periodic table. For defense applications, aerospace engineering, and advanced robotics, the most critical are Neodymium, Praseodymium, Dysprosium, and Terbium.

These specific elements are fundamental to the creation of magnets. Neodymium-Iron-Boron are the strongest known permanent magnets in existence, possessing exceptionally high magnetic fields in a specific, intended direction without wavering.

In military and defense contexts, these magnets are needed wherever mechanical torque or continuous electrical power generation is needed within a tightly constrained volume and weight limit. They actuate the tiny, speedy aerodynamic control fins on guided missiles, control the gyroscopic attitude of satellites orbiting the earth, drive the highly efficient electric motors in autonomous unmanned aerial vehicles, power advanced sonar arrays, and operate the electrical generators tucked inside the engine bays of fighter jets. All fairly important stuff, I’ll say.

While Neodymium and Praseodymium form the base of the magnet, Dysprosium and Terbium (Heavy Rare Earths) must be added to the alloy to increase the material’s resistance to demagnetization at extremely high temperatures. Because missile chassis and jet engine compartments experience massive thermal loads, a standard magnet would instantly lose its magnetic properties. The heavy rare earths prevent this catastrophic failure. Given that a single foreign adversary controls an estimated 70-90% of global rare earth processing and magnet manufacturing, this is clearly a glaring vulnerability for the USA and NATO.

Tungsten, Germanium, and High-Purity Silicon

The defense supply chain relies on a broader tapestry of specialized elements, each uniquely suited to extreme environments. Tungsten possesses the highest melting point of any known metal, turning to liquid only at an astonishing 3,422 degrees Celsius 🤯. It possesses a physical density comparable to that of radioactive uranium. Because of these properties, tungsten is entirely unmatched and irreplaceable for kinetic energy penetrators, and for the high-temperature superalloys used in the leading edges of hypersonic missiles and turbine blades of high-performance jet engines.

Germanium is a metalloid that is highly transparent to infrared light. While glass blocks thermal radiation, germanium allows it to pass through. Therefore, it is used to craft the actual physical lenses for the thermal imaging systems and night vision goggles discussed previously, acting in physical concert with the antimony based superlattice detectors. It is also a foundational substrate enabling solar cells that power satellites.

High Purity Silicon, now explicitly prioritized on the 2025 critical list, is the foundational, hyper refined substrate upon which all modern digital logic, memory chips, and artificial intelligence systems are etched. Without domestic silicon refining capabilities, the software and artificial intelligence algorithms developed by Western technology firms have no physical hardware upon which to execute their calculations.

Tantalum, Titanium, Cobalt, and Copper

Rounding out the physical materials necessary for defense dominance are metals required for structural integrity and energy transmission.

Tantalum is highly resistant to corrosion and is used to manufacture highly reliable, specialized capacitors used in the electronics of satellites, radars, and missiles that must endure extreme vibration and temperature fluctuations without failing.

Titanium is prized for its extraordinary strength-to-weight ratio and natural resistance to saltwater corrosion. It is the primary alloy used in the lightweight airframes of fighter jets, the pressure hulls of deeeeep diving submarines, and modern ballistic armor. The refinement of raw titanium ore into intermediate “titanium sponge” is a industrial choke point again heavily dominated by non-allied nations.

Though the graphic highlights REE dependency, an equally important factor used in these machines is Cobalt (Co, atomic number 27) which is a transition metal, not a REE. It’s classified separately as a critical mineral for defense. Cobalt is a crucial additive in the creation of superalloys for jet engines and gas turbines, ensuring they maintain structural integrity under intense centrifugal force and heat. It is also a vital component in the lithium-ion batteries that power military drones, portable soldier communication nodes, and space assets.

Finally (and this one isn’t a secret to anyone), copper, recently elevated to the critical list, is the literal nervous system of the defense apparatus. From the intricate wiring inside a radar array to the conductive cables required for base infrastructure, the surging demand for copper driven by tech and military needs has created severe supply shocks.

A Over-Promised, Under-Delivered Saving Grace: The Emergence of Graphene

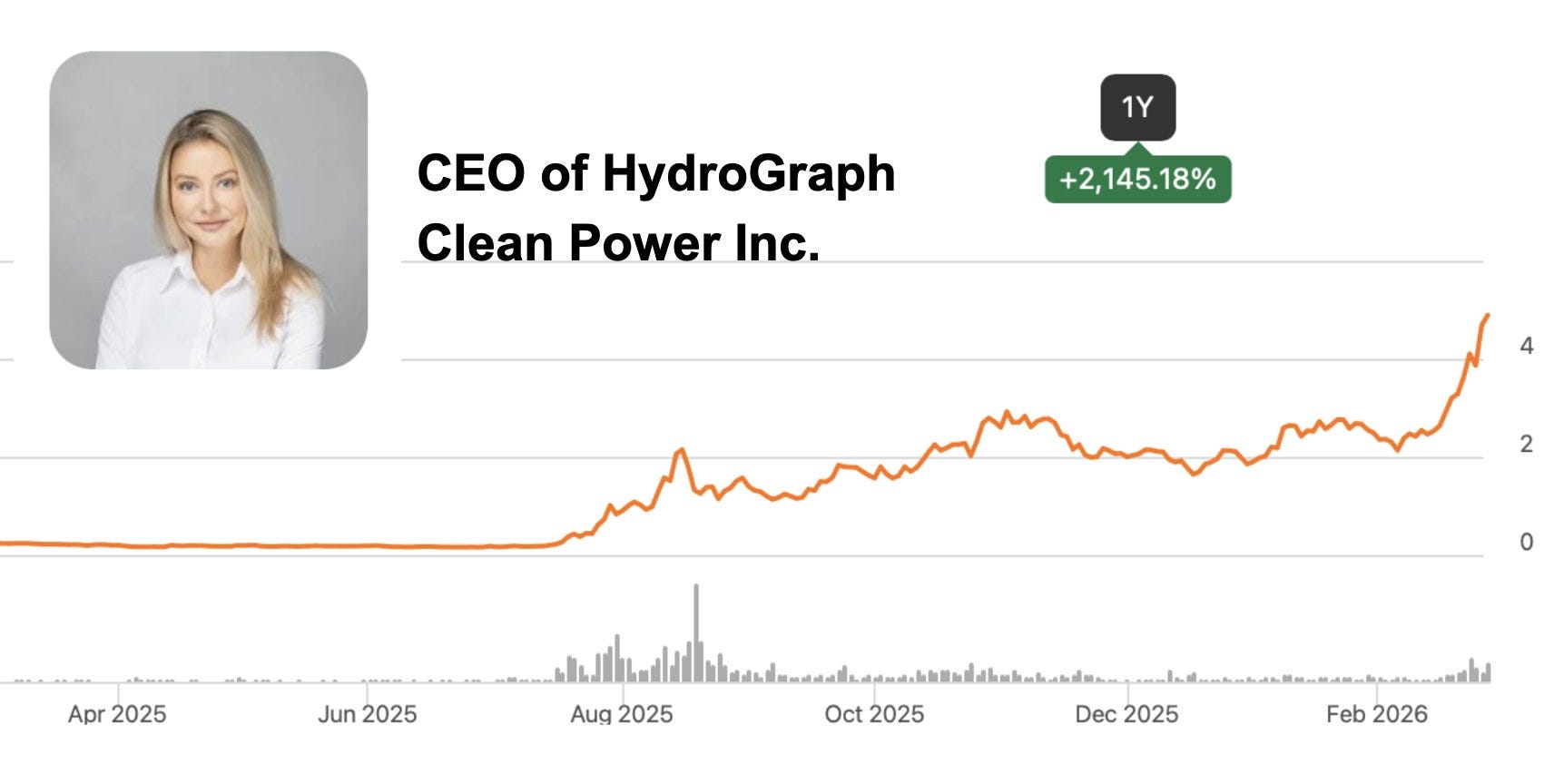

If Graphite is layers upon layers of Carbon, then Graphene is just one single layer. Known as a 2D single atom thick hexagonal lattice of carbon. With the growth of companies like HydroGraph Clean Power Inc. led by the Steve-Jobs like Kjirstin Breure, Graphene seems to be finally having its moment after 20+ years of remaining in the lab.

Graphene is shifting from theoretical physics to practical defense applications in 2026. It is stronger than steel, harder than diamonds, and exhibits superior electrical and thermal conductivity compared to copper, with vastly better electron mobility than standard silicon. Enabling fast charging of batteries, longer storage, and a plethora of other benefits.

Extensive research and military testing are validating graphene’s utility across several critical vectors. First, graphene nanocomposites are highly effective at absorbing and reflecting electromagnetic radiation. Applied as ultra-thin coatings to aircraft, naval vessels, or sensitive communication electronics, they provide essential electromagnetic interference shielding, protecting assets against electronic warfare jamming and the devastating effects of electromagnetic pulses.

Second, the development of highly conductive graphene inks and printed electronics allows for the creation of flexible, lightweight, and durable antennas. These antennas can be woven directly into a soldier’s tactical uniform enabling high frequency communications essential for the heavily networked battlefield.

Third, adding fractional percentages of pure graphene to thermoplastic resins increases the tensile strength and fatigue resistance of aerospace composites while simultaneously reducing weight of the material. This enhances the payload capacity / fuel efficiency / structural survivability of rockets, drones, and next-generation aircraft.

Operating in the highly specialized nanomaterials sector, HydroGraph Clean Power utilizes a patented, proprietary detonation process utilizing hydrocarbon gases to synthesize pure graphene. Synthetic. Unlike traditional methods that rely on the mechanical or chemical exfoliation of naturally occurring mined graphite, this detonation synthesis produces a turbostratic, fractal graphene with an astonishing purity level of 99.8 percent, featuring total crystallization. For comparison, this is much more pure than competitors, it seems.

Because the process does not require heavy mining equipment or massive chemical refinement vats, the company’s modular commercial production units require less CapEx while generating scaled volume. This cost-effective synthesis theoretically positions the company to supply the exact type of ultra-high-purity graphene required for next-generation defense applications, such as the aerospace composites and electromagnetic shielding discussed earlier, entirely bypassing the vulnerable overseas graphite mining supply chain.

More on Graphene: NanoXplore and the Broader Market

Operating as a volume leader in the North American market, NanoXplore produces thousands of tons of graphene powder annually. While focused heavily on commercial applications, the company provides standard and custom graphene-enhanced masterbatch plastic pellets and composites to various customers in the transportation and defense sectors. Alongside other equipment manufacturers and application developers, the maturation of these companies highlights the transition of the graphene supply chain from volatile laboratory experiments into reliable, industrial-scale production capable of supporting defense procurement.

We hope Graphene becomes as important as it’s sold to be. It would be a massive unlock for tech, defense, and electrification (EVs, batteries, etc).

Project Vault: The Sovereign Critical Minerals Reserve

Recognizing the severe threat posed by centralized global supply chains and export bans, the United States government took unprecedented economic action in early 2026. In coordination with the Export-Import Bank of the United States, the federal government launched a much needed initiative called Project Vault.

Project Vault is a $12B initiative designed to establish a domestic stockpile of critical minerals. Conceptually, it is modeled after the Strategic Petroleum Reserve, which was established in the 1970’s to protect the nation from oil embargoes. And is architected through public-private partnerships. The initiative is backed by a $10B loan authorization from the Export-Import Bank, plus $2B in committed private capital. Frankly, this should probably be 10x bigger, but I assume we’ll dollar cost average over time to avoid driving up pricing too quickly. That supply shock would’ve dismantle the entire point of doing this.

The overarching objective of Project Vault is to insulate domestic industrial base from abrupt foreign export bans, unexpected supply shocks, and the predatory price manipulation tactics historically employed by China. For example, China would flood the market to keep prices suppressed, thus allowing them to maintain position as the only financially justified location in the world.

By USA stockpiling heavily refined elements like gallium ingots, antimony trisulfide, and separated rare earth oxides in highly secure domestic facilities, the government helps justify local companies to continue production even in the event of dropping prices.

In other words, Project Vault functions as a market stabilization mechanism. Avoiding Global powers being able to bankrupt new ventures before they can achieve commercial scale. Vault acts as a well-capitalized buyer of last resort committing to purchase domestically produced critical minerals at the price floor. Thus ensuring domestic mining operations, like in Idaho, have a guaranteed off taker at a price that sustains their long-term scaling, permanently de-risking the immense capital requirements to operate new mines.

This initiative serves as the capstone of a much broader strategy. Over recent years, federal entities have issued billions in authorizations and letters of interest for domestic and allied projects. This includes hundreds of millions for domestic rare earth processing, massive loans for domestic lithium extraction from clay, and significant international financing to secure allied supply chains, such as copper and gold production facilities in South Asia. The overarching strategy is designed to create a allied focused architecture that bypasses choke points entirely.

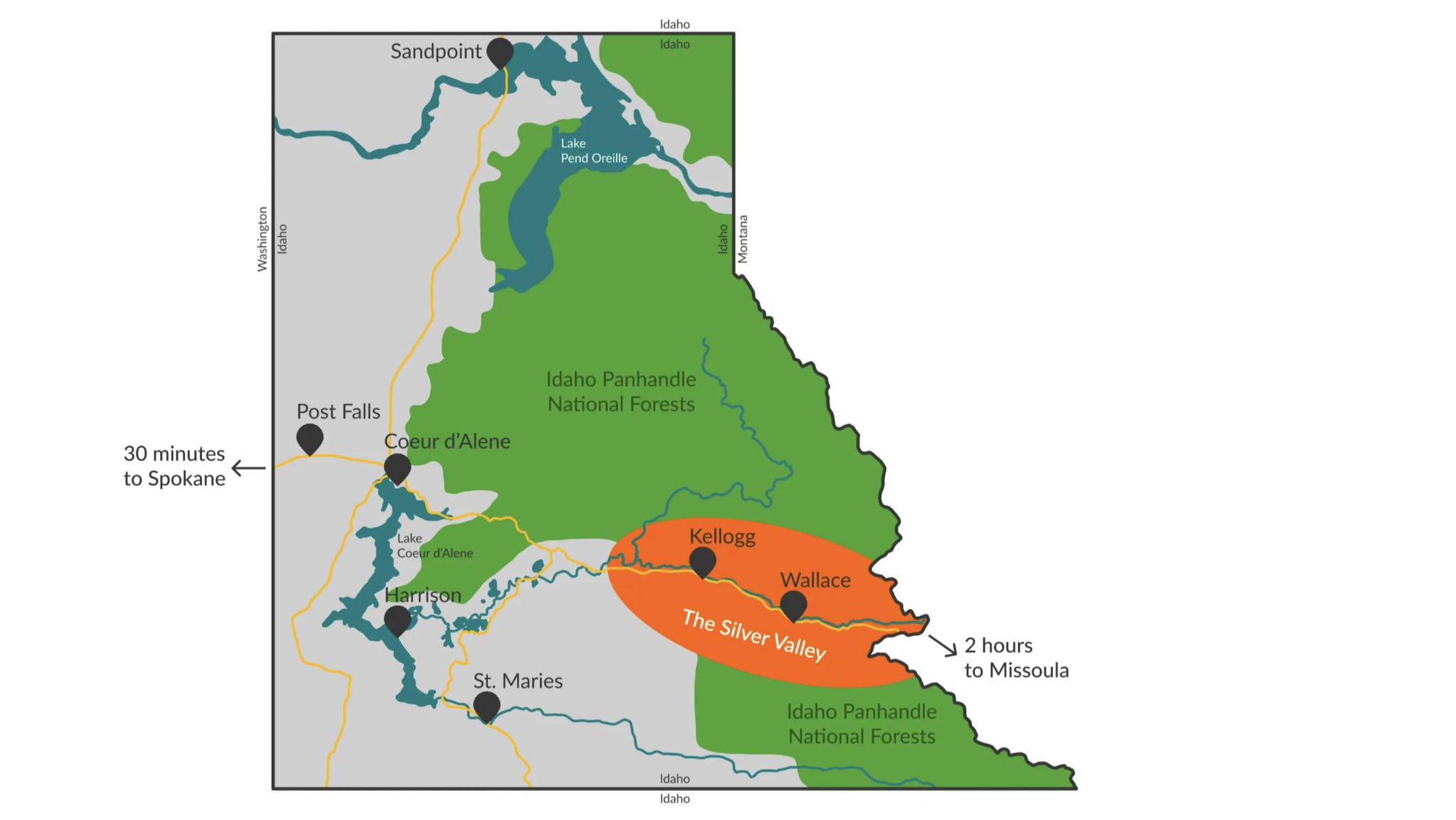

From Silicon Valley to Silver Valley: Reshoring the Physical Supply Chain in Idaho

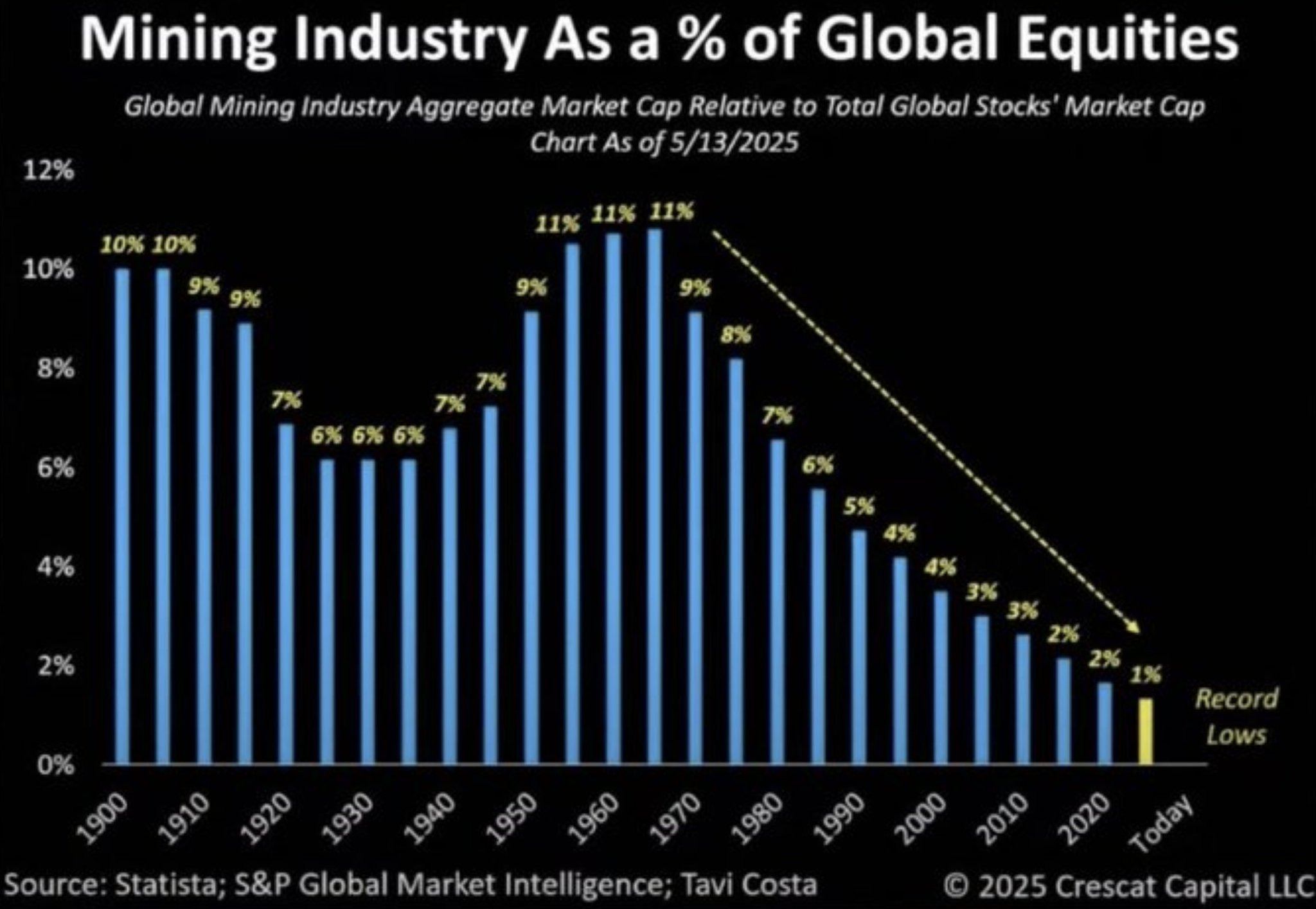

In 2026, a specific cohort of companies has emerged as the vanguard of this renaissance. But the scariest part, is that some of these ‘critical’ companies aren’t even doing revenue yet. You can see in the below graph, mining industry has been taking a hit for decades.

The USA is behind, but again, catching up quickly. Thanks to regions like Silvery Valley in Idaho.

Antimony and Silver: Highest Priorities

Perpetua Resources

Perpetua Resources is rapidly advancing the Stibnite Gold Project in the central region of Idaho. The Stibnite site is of paramount national importance because it contains the only known, economically viable reserve of antimony in the United States, hosting an estimated reserve of one hundred and forty-eight million pounds of the critical metalloid. Upon reaching operational maturity, Perpetua explicitly projects it will supply up to thirty-five percent of total domestic antimony demand during its first six years of full-scale operations.

They’ve lost $45M over the past 12 months, and aren’t even generating revenue. Yet, their success is very important. And this is why it’s critical we restore and reshore, fast!

Perpetua’s immense strategic importance is reflected in its tiered government backing. By the end of 2025, the company had received over eighty million dollars in direct federal funding. This includes capital injections under the Defense Production Act to advance construction readiness and permitting, alongside significant awards through the Defense Ordnance Technology Consortium. The company also secured term sheets for up to two billion dollars in potential debt financing from the Export-Import Bank.

On the technological front, Perpetua has entered a strategic agreement with the Idaho National Laboratory to host, commission, and operate a flexible, modular pilot processing plant. This plant is designed to receive material directly from the Stibnite project and produce high-quality, military-specification antimony trisulfide, bypassing foreign refining bottlenecks entirely and proving that the United States can produce the exact chemical compounds required for defense munitions domestically.

United States Antimony Corporation, and Americas Gold and Silver Company

This is a wonderful story about two CEO’s who only first met last month, and already have inked a joint venture deal (51%, 49%) to mine and process Antimony entirely in Idaho. JV was announced February 10, 2026.

United States Antimony Corporation owns and operates the Bear River Zeolite mine and processing facility in southeast Idaho (for zeolite, a different mineral used in filtration) but more recently, in February 2026, they announced a joint venture with Americas Gold and Silver to build a new commercial-scale hydrometallurgical processing facility in Idaho’s Silver Valley.

United States Antimony Corporation in late 2025, the company secured a monumental, quarter-billion-dollar contract with the Defense Logistics Agency to continuously supply antimony metal ingots directly to the national defense stockpile.

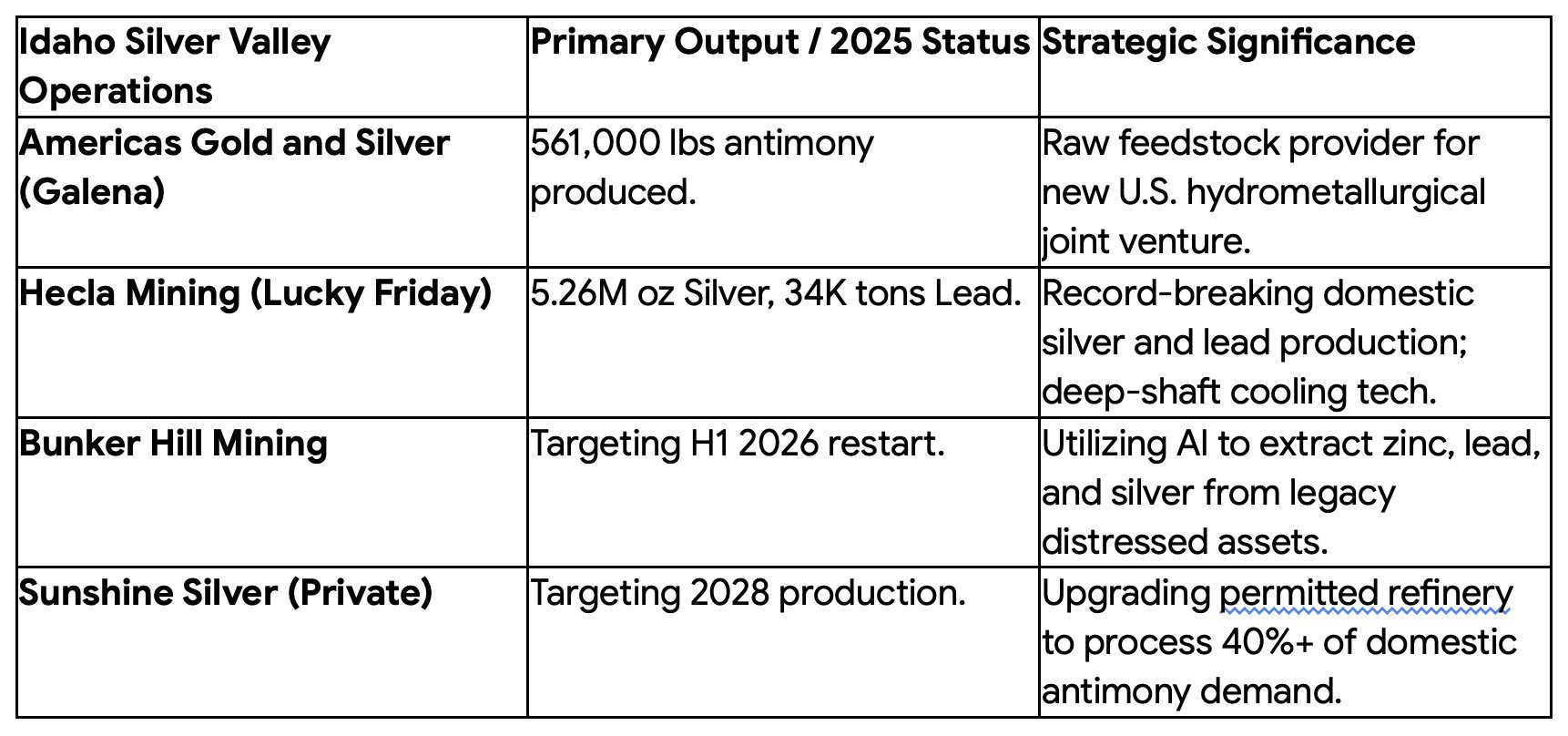

To secure the raw feedstock required to fulfill this government contract, United States Antimony entered a highly synergistic joint venture with Americas Gold and Silver. Americas Gold and Silver operates the fully permitted Galena Complex in Idaho, which successfully produced over half a million pounds of antimony contained in concentrate in 2025, alongside its primary silver output. Antimony being the byproduct in this scenario.

Previously, Americas Gold and Silver would ship it to Canada, and then United States Antimony Corporation would buy it, bring it back to USA, and refine it. This is dumb, and their new JV ensures no need for an over-priced middle man.

This partnership effectively creates a fully localized, closed-loop supply chain from the mine shaft directly to the military stockpile, utilizing American ore and American processing technology.

Sunshine Silver Mining & Refining

Operating in the private sector with heavy backing from major institutional investment groups, Sunshine Silver Mining & Refining closed a $75M equity financing round to accelerate the development of the historic Sunshine mine and its associated physical refinery.

The Sunshine refinery, which already benefits from hundreds of millions of dollars in legacy infrastructure, is fully permitted and currently being upgraded to specifically handle the complex processing of antimony. The company is targeting first large-scale production by 2028 (Yikes! So slow..). Because the facility is designed to process both its own extracted ore and third-party concentrates, Sunshine boldly projects that its facility could supply approximately 40% of domestic antimony demand by 2028, rising to as much as 80% in the following years. Not sure I buy it! The company also intends to integrate the production of highly gallium and germanium, creating a multifaceted minerals hub.

Bunker Hill Mining Corp.

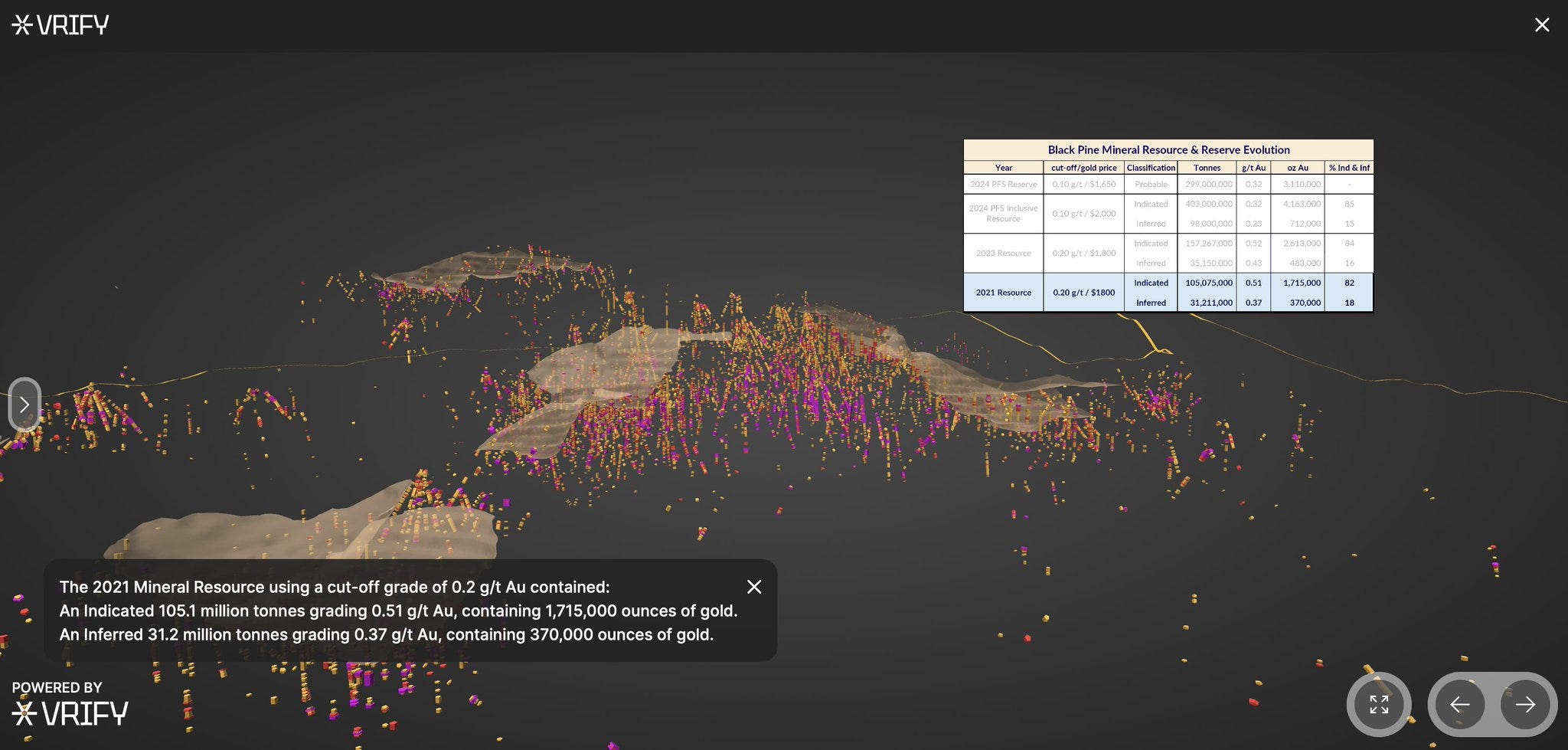

Also operating in the prolific Silver Valley of Idaho, Bunker Hill Mining is in the final stages of revitalizing the historic Bunker Hill Mine, aggressively targeting a full production restart in the first half of 2026. The company represents the modernization of legacy physical assets, transitioning from infrastructure rehabilitation to active mining preparation.

By the close of 2025, the company reported that its processing plant construction had reached 80%+ completion, with its critical tailings filter press advancing rapidly. What distinguishes Bunker Hill in the modern era is its deployment of AI. The company has actively integrated AI-assisted mineral discovery platforms to remap the historic underground workings, allowing their geologists to target higher-grade silver, zinc, and lead mineralization. By deploying AI to distressed assets, Bunker Hill aims to hopefully inject new life into the North American supply chain with substantially lower capital intensity than required for a new greenfield project.

I believe they partnered with VRIFY for the AI tech. Which offers the industry’s leading AI-assisted mineral discovery platform, including DORA for prospect mapping. It processes geospatial datasets with proprietary AI models to uncover mineralization patterns, generate targets, and support investor/regulator communication. Used by companies like Bunker Hill (for remapping historic workings in Idaho’s Silver Valley), Metallic Minerals, Nevada Sunrise, and Equinox Gold.

Hecla Mining

Hecla Mining, a dominant, long-standing player in the global silver sector, reported record-breaking production at its Lucky Friday mine in Idaho, achieving an astonishing output of over 5.2 million ounces of silver in 2025, alongside massive tonnage of lead and zinc.

Recognizing that the physical economy requires extracting minerals at increasingly extreme and hostile depths, Hecla has invested heavily in complex subterranean infrastructure. The company advanced a massive surface cooling project designed to deliver mechanically chilled air deep underground. This infrastructure is an absolute necessity to maintain safe, survivable working conditions for miners as operations advance deeper into hotter geological zones where the high-grade silver and lead are located. Furthermore, Hecla’s ability to navigate complex labor relations, securing a long-term union contract, ensures that this critical domestic production will remain uninterrupted through the end of the decade.

Rare Earth Elements: Breaking the Magnet Monopoly

The extreme vulnerability of the Neodymium-Iron-Boron permanent magnet supply chain has led to dramatic federal interventions to support domestic rare earth processing and downstream manufacturing.

MP Materials

MP Materials operates the Mountain Pass mine in California, which stands as the only active, scaled rare earth mine in North America. Historically, the company successfully mined the raw ore but lacked the complex domestic infrastructure to refine it, forcing them to ship the concentrated material to foreign adversaries for separation into individual elements.

To permanently break this reliance, the Department of Defense partnered with MP Materials in a transformational, multi-billion-dollar public-private package. The cornerstone of this partnership is a modified contract-for-difference agreement. The government legally guarantees a hard price floor of $110/kilogram for the company’s refined NdPr output over a 10 year period. In late 2025, when predatory global market prices dipped below this floor, MP Materials realized over $50M in price protection agreement income. This mechanism protected their margins, and USA independence, allowing the company to a shield from foreign economic implosion attempts.

You can read my full deep dive on MP which I wrote last month on X: https://x.com/compose/articles/edit/2019754152381820928

Simultaneously, MP Materials is aggressively moving downstream to capture the entire value chain. In early 2026, the company broke ground on a massive, 120 acre rare earth magnet manufacturing campus in Texas, called 10X. Aided by $100Ms in state incentives and federal loans, this facility is designed to produce 10,000+ metric tons of finished Neodymium-Iron-Boron permanent magnets annually, complete with closed-loop recycling capabilities. This single facility is intended to provide the magnets necessary to power defense drones, commercial robotics, and electric vehicles, backed by guaranteed long-term offtake agreements from major technology conglomerates.

USA Rare Earth Company

USA Rare Earth is advancing the development of the Round Top deposit in Texas, widely considered by geologists to be the richest known domestic deposit of the highly coveted heavy rare earth elements.

In early 2026, the company announced a multi-billion-dollar financing package. The government took a direct 10% equity stake in USA Rare Earth, acquiring millions of shares of common stock and equivalent warrants. This was paired with over $1B+ in federal debt financing and equivalent private equity investment. This unprecedented equity position guarantees intense government oversight and financial support to ensure the Round Top mine-to-magnet supply chain achieves full commercial operation by 2028, securing domestic access to materials completely unavailable outside of hostile nations.

Trilogy Metals and Ambler Metals: Upper Kobuk Mineral Projects in Alaska

Trilogy Metals, operating in a highly structured joint venture with a major global mining conglomerate, manages Ambler Metals. This entity controls the Upper Kobuk Mineral Projects located in the remote wilderness of northwestern Alaska, recognized as a world-class, high-grade deposit of copper, zinc, lead, and cobalt.

In late 2025, Trilogy announced a landmark investment directly from the Department of Defense’s Office of Strategic Capital. Mirroring the strategy deployed with rare earths, the government acquired an approximate 10% equity stake in Trilogy Metals, injecting $10m’s to advance the de-risking and exploration of the Arctic deposit.

However, this transaction highlights the immense complexities of reshoring heavy industry. The federal government’s dual role as both an incentivized equity shareholder seeking a return on investment and the supposedly impartial regulatory body overseeing the strict environmental permitting of the contentious access road required to reach the mine has raised profound policy questions. The joint venture is attempting to navigate these hurdles by leveraging expedited federal permitting frameworks designed to enhance coordination for critical infrastructure, balancing the absolute necessity of domestic copper production with stringent environmental protections and the livelihoods of indigenous communities.

Albemarle Co. and the Kings Mountain lithium project in NC

Focusing on energy storage, Albemarle is advancing the massive redevelopment of the Kings Mountain lithium project in North Carolina. Recognizing the necessity of domestic battery supply chains for both electric vehicles and specialized military communications equipment, the federal government awarded Albemarle massive grants, totaling hundreds of millions of dollars, funded through bipartisan infrastructure legislation.

These funds are explicitly directed to partially fund the design, construction, and operation of a massive mineral processing plant capable of producing hundreds of thousands of metric tons of spodumene concentrate annually. To address environmental concerns associated with heavy lithium extraction, Albemarle’s engineering plans include designing the mine to operate on a closed-loop water system utilizing collected precipitation, and actively developing secondary commercial markets for processed ore tailings to minimize the physical waste footprint.

The Execution Layer: Workforce Deployment

The strategic posturing, the billions in allocated capital, and the geological wealth of the North American continent are entirely useless without the physical labor required to build the infrastructure. Hydrometallurgical processing plants, rare earth magnet factories, deep-shaft mine cooling systems, and highly automated defense foundries must be physically assembled by human hands. To reshore the supply chain, the United States also must restore highly skilled tradespeople.

The deployment of this physical infrastructure relies heavily on specialized, publicly traded electrical and mechanical contracting conglomerates. These companies are experiencing unprecedented, historic growth, driven simultaneously by the massive push for commercial electrification, the explosive construction of data centers for artificial intelligence, and the desperate revitalization of the heavy industrial base.

The Heavy Industrial Constructors

The companies responsible for physically assembling these reshoring megaprojects manage workforces larger than many standing armies, organized under complex union agreements and rigorous safety protocols.

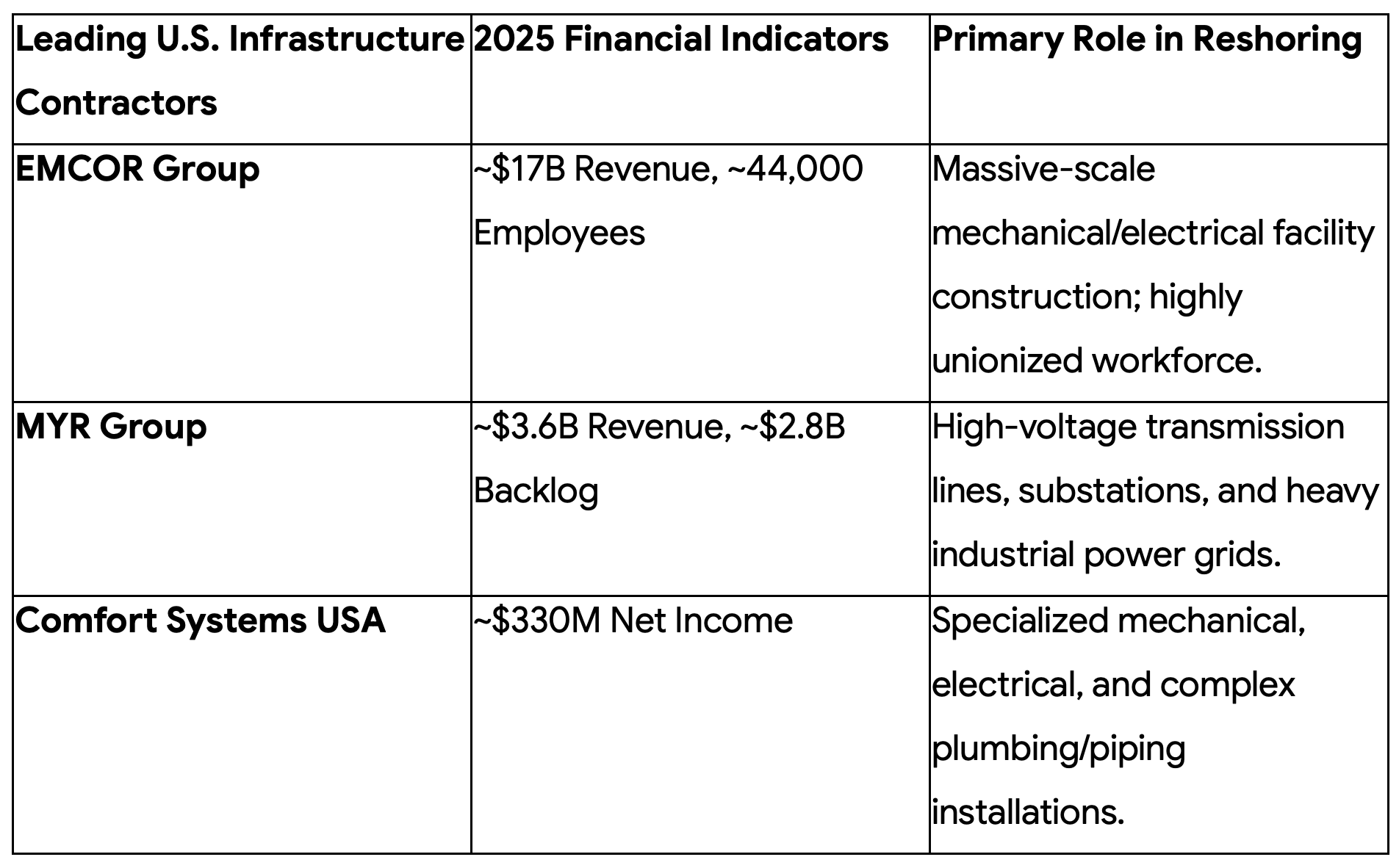

MYR Group

Operating as a premier specialty contractor serving the electric utility infrastructure market across North America, MYR Group reported record-shattering full-year revenues well in excess of three and a half billion dollars in 2025. More tellingly, the company reported an immense, multi-billion-dollar backlog of guaranteed work.

The company employs massive teams of highly trained electricians across two primary segments: Transmission and Distribution, and Commercial and Industrial. They are the personnel physically responsible for building the high-voltage transmission lines, complex substations, and dedicated clean energy projects necessary to provide the massive, uninterrupted electrical power required by heavy industrial processing facilities and high-vacuum semiconductor foundries.

EMCOR Group

Operating as an absolute titan in the mechanical and electrical construction sector, EMCOR generated revenues approaching seventeen billion dollars in 2025. This staggering financial output is supported by a massive, highly structured workforce of approximately forty-four thousand employees, the majority of whom are represented by labor unions under hundreds of distinct collective bargaining agreements.

EMCOR’s record remaining performance obligations underscore the immense, nationwide demand for complex facility construction, heavy HVAC integration, and power systems engineering. When a rare earth mining company needs to construct a billion-dollar, heavily ventilated, environmentally contained magnet manufacturing facility, they must rely on the structured deployment and project management expertise of conglomerates like EMCOR.

Quanta Services and Comfort Systems USA

Quanta Services continues to dominate the utility infrastructure space, frequently ranking as the largest electrical contractor by revenue. Recognizing the specific, specialized needs of the reshoring effort, Quanta recently acquired leading mechanical, plumbing, and process infrastructure providers specifically to strengthen its craft labor capabilities for the expanding technology and manufacturing markets.

Similarly, Comfort Systems USA, which provides highly specialized mechanical, electrical, and plumbing services, reported massive surges in net income, driven by the intense demand for the installation and continuous maintenance of the complex piping, fluid dynamics, and electrical systems required in heavy manufacturing and processing plants.

The Plumbing and Maintenance Layer

While the heavy industrial contractors build the mega-facilities, the broader physical economy requires constant maintenance of its fundamental fluid and waste systems.

Chemed Corporation (Roto-Rooter)

The plumbing and mechanical maintenance sector is highly fragmented, but conglomerates like Chemed, through its massive Roto-Rooter subsidiary, manage thousands of licensed plumbers nationwide. While operating more at the commercial and residential service level rather than heavy industrial construction, the management and continuous training of thousands of tradespeople highlight the vast scale of human capital required to maintain the fundamental water, drainage, and mechanical systems that keep municipalities and commercial hubs functional, allowing the broader economy to operate without interruption.

The availability of this skilled labor is the ultimate operational bottleneck of the entire physical economy. The speed at which a mining corporation can build an antimony processing plant in Idaho, or the pace at which a rare earth conglomerate can scale a magnet facility in Texas, is completely and entirely dictated by the availability, training, and deployment of the electricians, pipefitters, welders, and mechanical engineers.

Summary: Strategic Second and Third Order Implications

The restructuring of the United States’ physical economy in 2026 carries profound downstream effects to reshape continental landscapes for decades.

First, the direct equity investments by the federal government into publicly traded and private mining companies signal a permanent departure from traditional free-market principles within the defense sector. By holding equity stakes, the government has essentially created a class of sovereign-backed enterprises. This guarantees critical projects will not fail due to short-term commodity price fluctuations, as the state will utilize its vast resources to protect equity and national security. This of course is controversial, and definitely politicized.

This model also introduces profound regulatory complexities. The government is now operating as an incentivized shareholder seeking operational success and the regulator tasked with protecting public lands, creating a delicate tension between the speed of industrialization and ecological preservation.

Second, reshoring heavy industry, mining, and metallurgy is inflationary at face value, but with the right policies can be mitigated. Domestic environmental compliance, the utilization of unionized labor, the immense CapEx of establishing power infrastructure, and the strength of USD Western debt make American-produced antimony, rare earths, and electronics are more expensive to produce than foreign counterparts. That is the likely reality, but doesn’t necessarily mean this is incorrect. In fact, it might mean it’s just the medicine we must take to stay healthy over the long term.

Third, the immense difficulty, time delay, and capital intensity of permitting and opening new physical mines are forcing mining companies to adopt AI to target their drilling, maximizing resource extraction without expanding their physical footprint. Advanced materials companies are utilizing synthetic chemistry, such as detonation processes, to create superior materials like graphene from basic gases, attempting to bypass traditional terrestrial mining entirely. The constraints of the physical world are forcing software and artificial intelligence to optimize physical processes at an breakneck speed.

Finally, the sheer scale of the required raw materials dictates that domestic reshoring alone is insufficient to meet the demands of the defense and technological base. The formation of initiatives like Project Vault and the multi-billion-dollar international loan portfolios of federal banks illustrate the necessity of “friend-shoring.” The United States is actively establishing a deeply integrated, highly capitalized economic architecture with tightly bound allied nations designed to create a secure, walled garden of global supply chains that excludes adversarial monopolies from critical procurement networks. This is happening across copper projects in South Asia or lithium extraction in Australia.

Conclusion

The realization that the real economy is undeniably physical has fundamentally reshaped industrial policy, corporate strategy, and national defense posturing in 2026. The ethereal concepts of cloud computing, artificial intelligence algorithms, and invisible electronic warfare are unequivocally anchored to the ground by heavy metals, high-temperature metallurgy, and extraction of the Earth’s crust.

As adversaries have successfully weaponized their historical dominance over esoteric elements like gallium, germanium, antimony, and rare earths, the extreme vulnerability of the Western defense apparatus has been laid bare. Without these specific elements, advanced radar arrays go blind, thermal imaging systems go dark, permanent magnets lose their torque, and precision munitions lose their armor-piercing lethality.

In response, historic alignment of federal capital, defense policy, and private enterprise has emerged. Through market-making mechanisms like Project Vault, massive direct equity purchases by federal departments, and the heavy utilization of emergency production acts, the United States is rapidly attempting to reverse engineer 40 years of offshoring to build a resilient, localized supply chain. And btw, this injection into private sector isn’t any different than the Fed printing money to bail out banks, or FDIC ensuring banks are stable. So before you complain about what is happening with rare earths, think holistically. The Government support of important industries like mining, banks, and transportation has for a long time been fundamental to USA prosperity.

From mining companies navigating the incredibly complex permitting of Idaho antimony, to rare earth conglomerates executing vertically integrated manufacturing facilities in Texas, to the infrastructure giants deploying the 10,000+ of skilled tradesmen required to build it all... welcome to 2026’s geopolitical paradigm. The transition from a margin-optimized fragile economy to a resilience optimized model is messy. Yet, it is recognized at the highest levels of industry as an absolute strategic necessity.

In the geopolitical landscape of the late 2020’s, technological supremacy and national sovereignty are not won in the digital realm; they are extracted from the earth, refined in the furnace, and forged by tradespeople.

⚠️ DISCLAIMER:

I’m researching all of this because I’m searching for global trends for myself. I own stocks of companies mentioned in this article, and in NO WAY AT ALL should you take this as investment advice. I’m creating this as a way to help me learn. I am not an Einstein genius, so educating myself on where the world going is very important for my relevancy.

I write this as a way to learn, and I hope that you are also learning. If you have questions, or comments, please don’t hesitate to reach out or respond on X.

If you are reading this to learn, or for any other reason, that is great. But you MUST do your own diligence, validate all the data, study these things yourself. I am just one guy trying my best, I know nothing, and am attempting to learn in public.

I hope you take the time to read, learn, follow, and share this information with important people in your life.