Adobe (ADBE) — Thoughtful Memo

Initial Allocation: 1.5 - 2.5% | Confidence: 7/10 | Memo Completeness: 8/10 I Net Score: ~7/10

Disclaimer: This is a note I’m writing to myself, I do this to help me think through MY OWN investment decisions. You should not take any of this as advice for your own investments, each investor is different, and each situation requires different risk appetite. YOU MUST DO YOUR OWN DILLIGENCE. I’m happy to discuss how you’re thinking about this, just leave a comment, or DM me on X.

Analysis Preview:

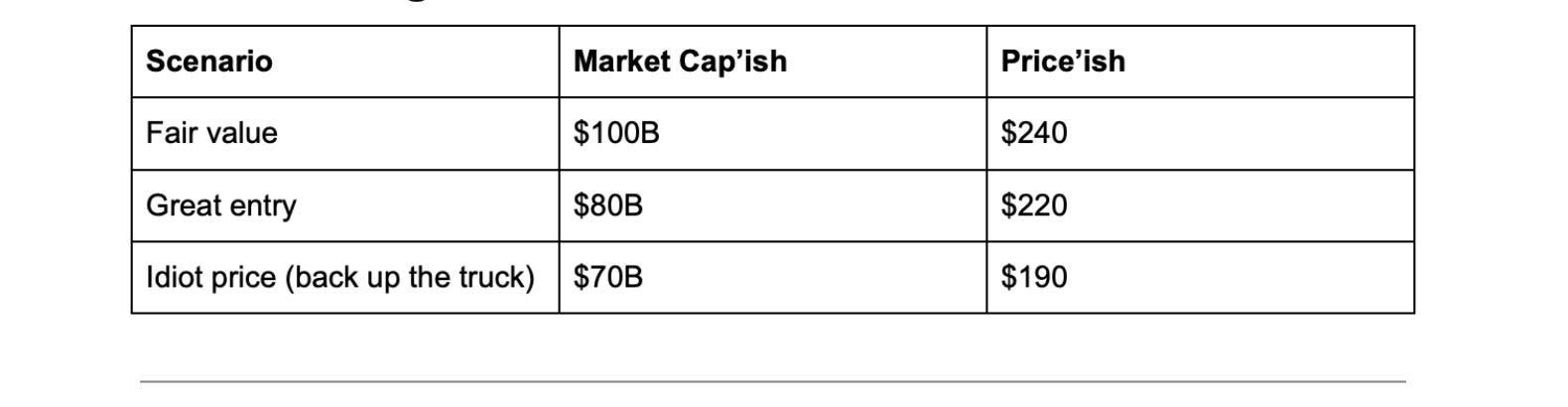

Personal Valuation Targets

Context:

Falling Knife? Or, Fallen Angel?

The AI narrative of AI Design tools x Job Displacement is causing investors to fear Adobe is losing pricing power, and will also lose their customer growth/retention advantages. The stock technicals make you think this is a falling knife. The business fundamentals make you think this is a fallen angel.

THESIS:

I think this is a Fallen Angel.

Adobe turns retained earnings into more growth, leading to a compounding flywheel. I feel they will retain leadership in an AI world, they’ll charge on a usage basis in addition to a per seat basis, and the macro narrative around AI design and AI job displacement will become tailwinds at some point.

Business Fundamentals + Valuation Overview:

Adobe halved its top line growth rate in 2022 from 20% to 10% and never recovered, but it stabilized its NI margin around 25% (actually closer to 30% on clean quarters) and continues to still grow revenue consistently at ~10%.

Real numbers (TTM through Feb 2026):

Revenue $24.45B

Net Income $7.21B (NI Margin ~29.5%)

Market Cap ~$99B, P/E 14.25

Applying 10% revenue growth: new revenue $26.9B, new NI at 29.5% margin = $7.93B, market cap at same 14.25 PE = $113B. That’s a 14.1% return — below the 15% goal, but after a 33% handicap, still ~10%. In the worst case, Adobe could reduce compounding from 15% to 5% and still deliver treasury-like returns.

Rating: 6/10

The Core “Not-Stupid” Argument (7/10)

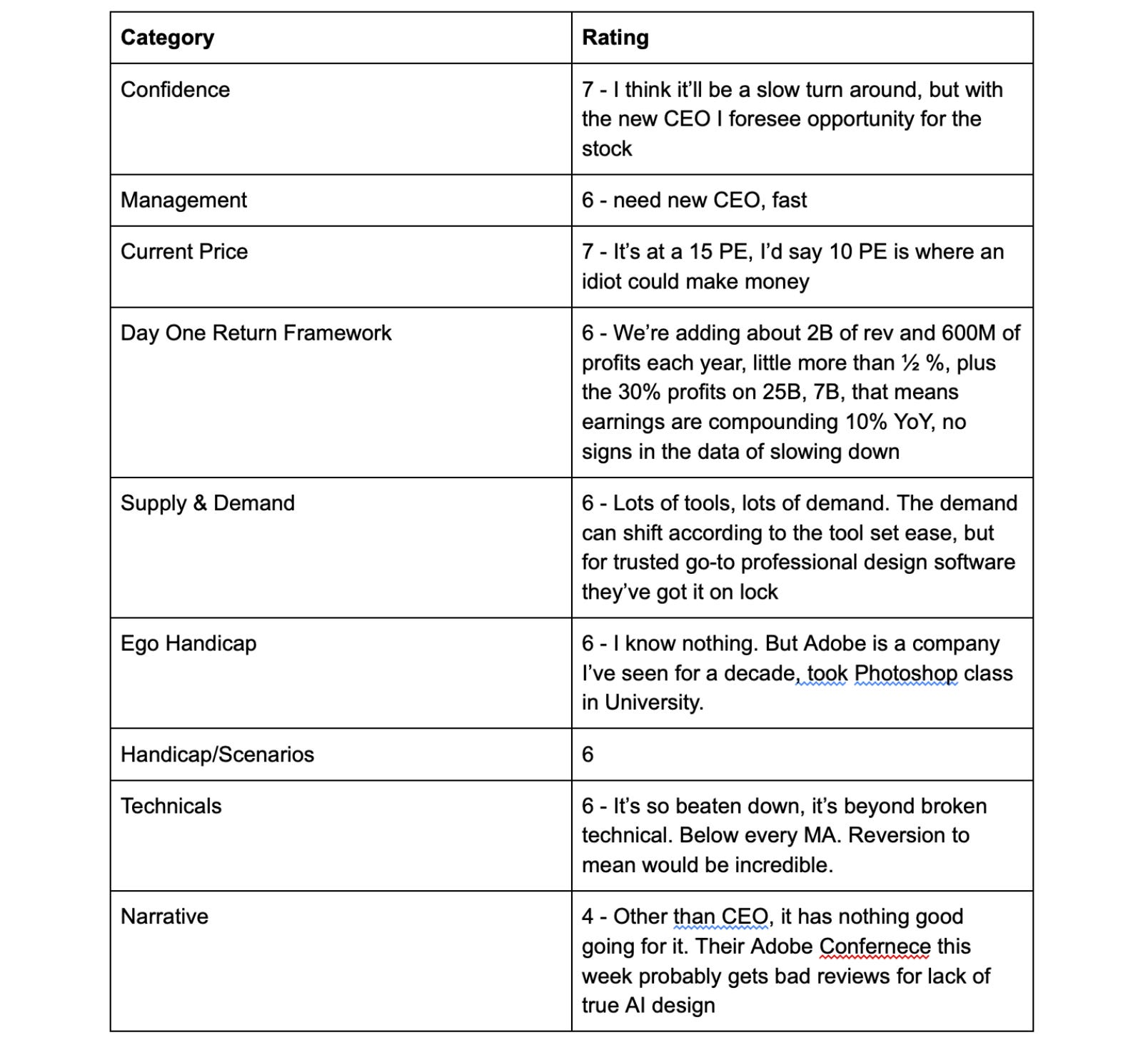

Buying Adobe is stupid because we can’t predict the future with AI, but every risk is an opportunity. Adobe isn’t going anywhere any time soon. It’s historically out-of-favor at a 15 P/E and 10x OCF/E, and the stock is back to its 2019 price. Do I really think AI is going to impact this so negatively that it’s now in a worse position than it was pre-COVID? No chance.

The “not-stupid” move is delegating a small amount into Adobe and tracking to confirm the thesis doesn’t get proven untrue. If we’re here in 18 months and Adobe has an AI Firefly product with $B’s of recurring revenue and they’re the leading AI design platform, I would have no problem believing that.

I could be very wrong, but at this discount, passing on this opportunity is a mistake, and going in too big too soon is a mistake. So let’s scale in. I believe this is a total winner despite CEO and AI headwinds.

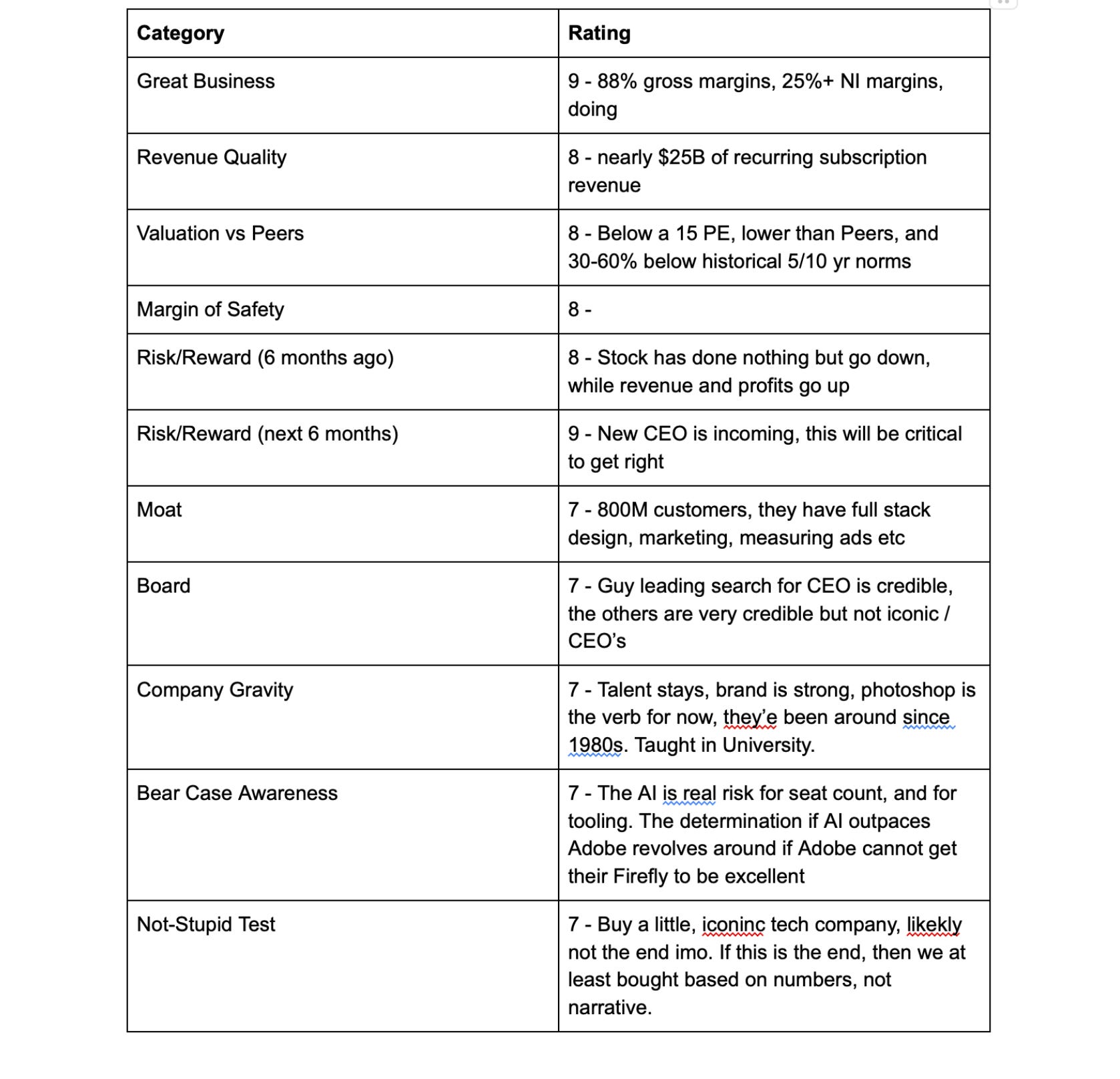

Is This a Great Business? (9/10)

Yes. Founded in 1982, this company had the foresight to build software for printing and digital publishing. They’ve been through the ringer — desktop to CDs, to the cloud pivot, and from one-off to subscription model (now doing almost $25B in ARR, growing 10%). Tech companies evolve; that’s what they do.

Adobe grew its AI-related revenue 3x YoY and will launch a new “pay per usage” payment model. Frankly, I love it — it’s going to make the price for AI design cheaper and the ecosystem stickier. Adobe has so much going for it across both customer segments.

Revenue Quality (8/10)

Every single metric is going up and to the right:

Revenue grew 12% last quarter

850 million MAUs, growing 17%

ARR at $25.2B, growing 11.5%

RPO at $22.5B, growing 13%

AI-first ARR more than tripled YoY

Gross margins still 88%

FCF still $10B+

90% of revenue is recurring

What more can I say?

Moat (7/10)

This is taught in University, it’s built a brand over decades, it’s the go-to for professional designers.

Adobe is still growing 10% on a $20B+ top line — show me where AI is eating this business. There is zero evidence in the financials. Not in churn, not in revenue growth, not in ARR adds, not in user counts.

You’re paying 10x free cash flow for a business still compounding revenue in double digits, with 88% gross margins, on a predominantly recurring subscription base with low churn. That is not a value trap. That is not a declining business. That is a growing cash flow machine being priced like something is broken.

The market has taken a business growing 12% with 88% margins and priced it at 10x FCF because of a vibes-based thesis. And sure, some things are broken — but it’s not AI sensitivity, it’s management. And they’re getting a new CEO.

The three key risks to mitigate:

They select a shitty CEO

AI absolutely destroys design

The stock price doesn’t recover for years and they just keep burning cash on buybacks

The wild thing: Adobe was at $688 eighteen months ago. If you told someone in late 2021 they’d be able to buy this business at $244 while revenue nearly doubled from $16B to $24B, they’d think you were insane. The business has gotten meaningfully better while the stock has gotten 65% cheaper.

Small buy to begin, bigger buy if they bring in the right leadership. AI is a risk, but I contrarily think it’s more of an opportunity.

Current Price Thoughts (7/10)

Would I pay $100B for Adobe?

~$24B in revenue growing 10-11%. ~$10B in annual operating cash flow. ~88% gross margins. Dominant market position in creative tools. $25B in ARR deeply embedded in enterprise and professional workflows. ~850 million monthly active users.

This $244 stock price is historically low. It has historically not stayed at sub-15 PE very long — this is usually the low point.

Q1 FY2026 numbers: $3.04B in Operating Income (12% YoY increase), roughly $2.92B in FCF for the single quarter. Annualized, that’s an $11.6B+ FCF run rate for 2026.

Current valuation metrics: Under 14 PE. EV/Sales = 4x. 10x P/FCF. Growing revenue 10%. Growing EPS diluted 12%+. P/S is 4x — usually closer to 10x.

Capital allocation concerns: They spent $32B over four years on buybacks. At today’s stock price that money could have retired ~131 million shares instead of however many they actually got at inflated prices. Or it could be sitting as cash, making Adobe one of the most financially impregnable software companies on earth. Instead, equity has been hollowed out, working capital is negative, and the stock is down 65% from the highs they were buying at. The board authorized a $25B buyback program through March 2028 and has already completed $14.9B — burning through 60% of a four-year authorization three years early.

The CEO grew his comp 40% because it’s tied to EPS — so his comp went way up, shareholders went way down. Get this guy out of there.

Revenue visibility: RPO is $22B+ (65-68% current), giving strong visibility into contracted revenue over 24-26 months. Unearned revenues grew from $2B to $7B over the decade as multi-year contracts landed.

Supply & Demand Dynamics (6/10)

Design could become more commoditized — more slop means less value per design. But you can’t decrease the value of “good design.” Good design is good design.

If AI evolves from slop to good AI design, that increases supply of tools but should also increase demand for those tools. Products will likely become more specialized (like Suno with music, Canva with design).

Segment breakout (FY2025):

Creative & Marketing Professionals: $16.3B

Business Professionals & Consumers: $6.5B (growing 16% YoY to $1.8B in biz tools, marketing segment growing 12% to $4.8B)

Yellow flag: They just started breaking out segments into two clean buckets. I think they’re bunching stuff to cover up slow growth in the pro design segment. The underlying math isn’t as clean as the titles suggest.

Competitive Landscape & Peers (8/10)

Probably by far the best company out of the bunch, and one of the best values too.

Figma — massively unprofitable, barely profitable on OCF basis, 50x multiple

Canva (private) — $4B ARR at $42B valuation. Adobe has 8x the ARR and only 2x the valuation. Canva isn’t stealing Adobe’s core professional user — it’s serving the SMB marketing manager who was never going to buy Creative Cloud. Different market.

Autodesk — less than half the revenue but more than half the valuation. Better growth, legit business doing real net income. 50x PE but 25x OCF/E.

DocuSign — below 10x OCF/E and unearned revenue growing (4x equity). But PE is 25x because nearly 20% of revenue is SBC. Versus Adobe at ~8% SBC/revenue. (Cloud software average is 21%.)

Midjourney — $500M revenue is impressive for 200 employees, but it’s a prompt-based image generator. It doesn’t do video editing, PDF workflows, vector illustration, motion graphics, layout design, photo retouching, or any of the hundred other things Adobe’s suite does.

Management (6/10)

Hope they select David Wadhwani as CEO — he’s excellent. Not happy with how much money previous management blew on buybacks. Adobe should have way bigger hitter power players on the board, on par with ADP’s.

Lara (CMO) is solid — proven track record at Amazon (Worldwide Prime), Visa (NA Marketing), Nike, and Intuit.

Board & CEO Search (7/10)

Calderoni leading the CEO search. He was CFO of Red Hat, sits on boards of PANW and Adobe. Silicon Valley native.

Internal Candidates

#1 David Wadhwani (leading candidate) — Currently President of Digital Media, public face of Adobe’s AI integration strategy. Worked at Adobe 2005-2015, left to be CEO of AppDynamics within Cisco, Venture Partner at Greylock, then rejoined Adobe 2 years ago as CBO. CS degree from Brown. This dude is IMPRESSIVE.

#2 Anil Chakravarthy — Successfully ran Informatica as CEO (2015-2020), pivoting to cloud-first subscription model. Hit $1B+ recurring revenue. Laid groundwork for Informatica’s re-IPO in 2021 and eventual Salesforce acquisition.

External Wild Card

Jim Whitehurst — The phone call Calderoni makes first. Calderoni was Whitehurst’s CFO at Red Hat (2015-2017). Currently MD at Silver Lake, Executive Chair at Unity Technologies, chairs Qualtrics board. Scaled Red Hat from niche open-source to first multi-billion dollar open-source firm and orchestrated $34B sale to IBM. Executive Chairman at Unity gives him direct creative software experience. Seen as a turnaround specialist — exactly what Adobe’s stock chart is begging for.

Low probability, but the fact that Calderoni leads the search, Whitehurst is at Silver Lake, and Adobe’s stock is at 5-year lows creates a once-in-a-decade alignment of people, price, and positioning. Calderoni is essentially a Silver Lake alumni (CEO of Anaplan, which Silver Lake took private for $10.7B).

Wild thought: The smartest thing would be for someone to take Adobe private — cut the pointless spending, let cash flow pay off debt, own a nice asset forever. ~$13B/year in cash available for debt paydown if you add FCF plus remove buybacks.

Company Gravity (7/10)

It’s THE brand. Market leader. Iconic tech company with decades of proven sustainability. The new CEO will be extremely tell-tale — it’ll show how much gravitational pull this company truly has. If they get a winner, excellent. If they select David, also great — he returned for his second term after 10 years away. The company’s gravity did prove to draw him back in.

Margin of Safety (8/10)

The margin of safety comes from current valuations vs historical norms:

Average PE over last 17 quarters: 35x

Average PE over last 4 quarters: 24x

Current PE: ~15x

If it reverts to longer-term mean → ~100% margin. If it reverts to shorter-term mean → ~66% margin.

The business is not declining — growing revenue 10% with ~30% margins. So the PE shrinks over time naturally as earnings grow.

Based on historical norms, this is the best opportunity window in a decade. But it could be a value trap.

Ego Handicap (6/10)

IMPORTANT: This fundamentally rests on the bet against the AI job displacement trend. I don’t buy it — I think businesses will always need people. If design really does change that much, Adobe will be at the forefront. So either the AI displacement thesis is overhyped and Adobe is fine, or the AI design trend is so important that Adobe naturally will be there leading it. If this fundamental claim is wrong, almost none of my other work matters.

I definitely don’t know all I could. Been studying for 1-2 months. The price is getting close to irresistible. But I barely understand their full revenue mix, have many products to learn, and I’m only guessing at the next CEO. There are blind spots I’m not aware of.

Scenarios & Handicap (6/10)

Bull: Adobe becomes the leading AI design player through acquiring, building, and integrating. Reverts to favorable sentiment and re-rates to 25x PE. We retrace the 50%+ margin of safety back to average.

Base: Grows revenue 10%, keeps NI margin above 25%, finds strong but not iconic CEO, continues shifting focus onto AI design tools. Hovers around 15-20 PE.

Bear: AI tools and decreasing seat count accelerate. Customers start reducing purchase size and find other preferred tools, driving Adobe’s pricing power lower. Unbundling mess that never gets above 15 PE — meaning we purchased right when there was no hope left.

Bear Case (7/10)

They select a shitty CEO

AI absolutely destroys design

The stock price doesn’t recover for years and they just keep burning cash on buybacks

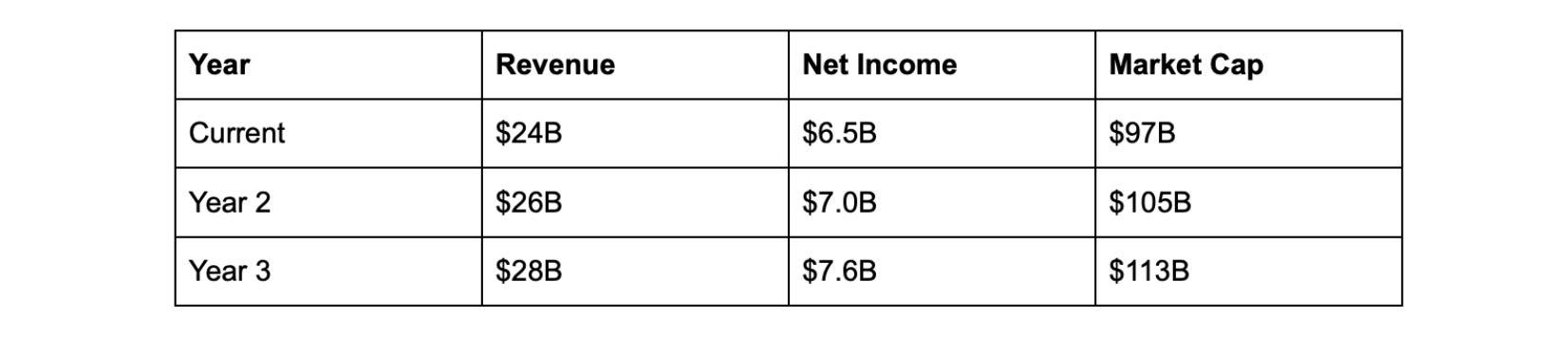

Forward Earnings Projection

Assuming 10% YoY revenue growth, ~27% NI margin (conservative), 15 PE:

Baseline: stays here for 3 years. Optimistic: AI story becomes tailwind, growth accelerates. Pessimistic: revenue stays similar but re-rating gets increasingly negative toward 10 PE.

Recent Results vs 6 Months Ago (8/10)

Numbers all grew. Market cap decreased. AI threat isn’t showing any dent in their growth yet — moving toward an all-clear personally, but definitely not there. Tread cautiously.

The price went down, the business went up.

52-week high: $422.95 (May 2025)

Six months ago (Oct 2025): ~$380-400 range, ~$160-170B market cap

Current (Apr 2026): $98.8B market cap — down 39.5% in one year while revenue grew

Next 6 Months Risk/Reward (9/10)

YES — when they select a new CEO, that one decision will be critical for the next 1-10 years, potentially more.

Technicals (6/10)

The stock never recovered from 2022. About as ugly a sustained downtrend as you can imagine since the Dec 2021 ATH.

Last time the stochastic was this low on a 5-year chart (2022), it went on to grow 2-3x over 2 years. The 2022 downtrend stopped almost exactly on the long-term moving average. The current downtrend just hit and stopped on the next MA below. If this MA acts as a floor → bullish. If it acts as a roof → we’re going down further.

Over the 3-month short term, we’re below every single MA. On a 10-year chart, this thing has fallen off a cliff.

The technicals make you think this is a falling knife. The fundamentals make you think this is a fallen angel.

Narrative (4/10)

The narrative is very against it. The macro narrative around AI design and AI job displacement are both headwinds. Firefly is going for it but unlikely to be material anytime soon.

Near-Term Outlook

1 day: Probably down

1 week: Adobe conference upcoming — doubtful they unveil anything material in AI

1 month: Lack of AI innovation at conference + Claude Design overhype could push this down more through April/May

1 year: Doesn’t report next earnings until June

Position Management

Initial buy: 0.4% allocation

Scaling triggers:

Need to know the NEW CEO

Need to see JUNE EARNINGS

Need to see if anything important happens at ADOBE CONNECT CONFERENCE

Need to monitor usefulness of AI design tools

Sell triggers:

Job growth turns and sustains negative

AI eats all of design — can just chat with an AI designer instead of needing Adobe

Entire market moves away from Adobe — customers leaving, decreasing spend

New CEO isn’t someone I believe in (vetted, not just taste)

Debatable but realistic: CEO search drags on for a year, company goes sideways, gets forgotten

Stop loss: No

AI”s BEAR CASE + My Rebuttal:

“I’ve read your full memo. You’ve done serious work. But here are the holes I’d rip into if I were sitting across from you trying to talk you out of this.”

Hole 1: Your “no evidence AI is eating this business” claim has a shelf life — and it might already be expiring.

You say “show me where AI is eating this business.” Fair — the financials look clean today. But that’s exactly how disruption works. Kodak’s revenue grew 5% the year before the cliff. Blackberry grew revenue 36% in fiscal 2011. The financials are the last thing to break. What breaks first is mindshare, new customer acquisition, and the talent pipeline choosing to build on other platforms.

Here’s what you should actually be scared of: Adobe’s user growth (850M MAUs growing 17%) is increasingly driven by Express and Acrobat — the low-end, document-side products. The professional creative core (Photoshop, Premiere, After Effects, Illustrator) isn’t being disaggregated in reporting anymore. They restructured segments this year into “Creative & Marketing Professionals” and “Business Professionals & Consumers.” You flagged this yourself as a yellow flag. You’re right to be suspicious. When companies stop breaking out their legacy core, it’s usually because the core is decelerating and they want to blend it with something faster-growing.

IF IT DOES DECLINE AND SLOW, WE’LL KNOW, AND WE’LL NEED TO SELL. BUT AS OF TODAY, THE REWARD IS GREATER WITH CONTRARIANS ON THIS ONE.

Hole 2: You’re buying the buyback damage, not avoiding it.

You correctly identify that management destroyed value — $32B in buybacks at inflated prices, negative equity, negative working capital. But you’re treating this as a past mistake that a new CEO will fix. The problem is the damage is already done and it’s structural. Adobe hollowed out its balance sheet. If the stock stays flat or declines further for 2-3 more years, they have fewer financial levers to pull than any of their peers. No war chest for transformative acquisitions. No cushion if there’s a downturn. You said yourself — if they’d kept that $32B as cash, they’d be “one of the most financially impregnable software companies on earth.” They didn’t. You’re buying the weakened version.

A new CEO inherits a company with negative tangible equity, $12B in goodwill, and a board that just authorized another $25B in buybacks. What if the new CEO is pressured to keep buying back stock instead of investing in AI? That authorization is a signal of board intent, not just an option.

TRUE, BUT THERE’S A WORLD WHERE THIS RETURNS TO 500/SHARE IN A COUPLE YEARS, AND NOW THOSE BUYBACK PRICES WERE SMART.

Hole 3: The 10x FCF is misleading because FCF includes SBC.

You keep anchoring on “10x free cash flow.” But Adobe’s reported FCF includes ~$2B of stock-based compensation flowing through as a non-cash add-back. You even note this — “removing that from OCF it’s $8B, about a 13x multiple.” So the real FCF multiple is 13x, not 10x. Still cheap historically, but not the screaming bargain you keep framing it as. And 13x for a company growing 10% with a CEO departure, AI uncertainty, and negative equity is... honestly pretty rational.

13X IS STILL INCREDIBLE FOR ADOBE. IT’S BEEN ABOVE A 20 ALL DECADE LONG PRIOR TO THIS.

Hole 4: Your “contrarian” bet isn’t actually contrarian — it’s consensus.

You say “no other investors seem to agree with me.” But 83% of Adobe is owned by institutions. Vanguard, BlackRock, State Street — they haven’t sold. The stock is down because multiple compression happened across all software, not because smart money abandoned Adobe specifically. You’re not buying something the market forgot about. You’re buying something the market has deliberately re-rated because the forward outlook changed. Every single sell-side analyst can run the same “15 PE on $7B earnings” math you can. They’re choosing not to pay that multiple. Maybe they know something you don’t about the next 3 years of seat-based pricing erosion.

THOSE FUNDS INDEX, THIS IS CONTRARIAN VS THE MARKET AS THEY REPRICED ADOBE, MY THESIS BELIEVES THEY SHOULDN’T HAVE BEEN RERATED DOWN SO MUCH ON MULTIPLES.

FUNDAMENTALLY, I BELIEVE AI ENHANCES CREATIVITY. IT’S A TOOL TO UNLOCK IT, MAKE IT FASTER, CREATE MORE EFFICIENT. JUST LIKE SUNO AND MUSIC.

“Creative Cloud has reached an estimated 41 million subscribers, nearly double the number from five years ago, up 4.24 million from last year. The ProDesignTools run rate is over 1 million new subscriptions per quarter — adding roughly 11,600 net new paid members every day.

That trajectory: 22M (2021) → 26M (2022) → 30M (2024) → 33M (mid-2025) → 41M (end of 2025). Seats are growing. Not stalling. Not declining. Growing 2-4M per year consistently.

But here’s the problem with that number: Adobe has never broken out professional Creative Cloud seats vs. Express/Firefly/Acrobat-bundled seats. That 41M almost certainly includes a ton of low-ARPU users on cheaper plans. The $15/month Express subscriber and the $55/month All Apps subscriber both count as “1 seat.””

THIS IS TRUE, BUT ALSO THE MARKET FOR $15 IS WAY LARGER, WAY MORE SEATS UP FOR GRABS IN AN AI WORLD AS MORE PEOPLE START SMALL BIZ.

The numbers are staggering:

5.62 million new business applications were filed in 2025, and so far in 2026 applications are up 25.54% compared to the same period last year. Finder

Pre-pandemic baseline was ~3.5M/year. We’re running at 5.5M+. That represents a 47.8% increase from 2019. Commerce Institute

So roughly 2 million MORE businesses per year are being formed now versus pre-COVID. Every single year. And it’s accelerating.

Now think about what every new business needs on Day 1:

A logo. A website. Business cards. Social media templates. A PDF contract. An invoice. Marketing materials. A pitch deck. Product photos edited. A brand guide.

Every single one of those tasks touches an Adobe product — or a competitor to an Adobe product. The point is, the TAM for design tools isn’t shrinking. It’s exploding.

–

Hole 5: The CEO catalyst is a coin flip, and you’re pricing in the upside without the downside.

You rate the board a 7, but your entire thesis hinges on who gets picked. You’ve built an elaborate narrative around Whitehurst and Silver Lake — but your own memo says this is “low probability.” If they pick Wadhwani (which the reporting suggests they already have), you get continuity. Continuity is fine, but it’s not a catalyst. The stock doesn’t re-rate on “same strategy, different face.” And if the search drags on — which you flag as a realistic scenario — you’re sitting in dead money for 6-12 months while the AI narrative gets worse.

LOOKING AT THIS ON A RELATIVE BASIS, THE NEXT CEO CAN’T BE WORSE THAN MISPRICED BUYBACKS! SO SURE, WE COULD STAY THE SAME, IN WHICH CASE I STILL THINK ADOBE RERATES BC AI HELPS CREATIVITY. AND A SMALL % CASE HE’S WORSE, BUT PROBABLY WILL JUST BE THE SAME. AND SOME % HE’S BETTER.

Hole 6: The Canva/Midjourney comparison cuts the wrong way.

You dismiss Canva by saying “a marketing coordinator making Instagram posts was never an Adobe customer.” But that’s the entire point. The TAM for “design” is exploding because of these tools, and none of that growth is flowing to Adobe.Adobe’s addressable market is getting bigger, and they’re capturing zero of the incremental demand. That’s not a sign of moat strength — it’s a sign of product-market drift. The professional designer market is mature and saturated. The growth is all in democratized design, and Adobe is losing that war despite having a 40-year head start.

REAL RISK VS CANVA. What to demand from Adobe in June earnings: BPC segment growth rate. If it accelerates from 15% toward 20%.

BUT, THIS IS A VALUATION BET. IF CANVA IS VALUED AT 45B, ADOBE 100B, YET ADOBE DOING 20B REV SO 5X SALES, AND CANVA 11X SALES ON 4B REV, MAKING ADOBE MORE SAFE, BUT MAKING CANVA A GROWTH PLAY. HOWEVER, THERE WILL BE AT LEAST A 1-3 YEAR PERIOD WHERE ADOBE CAN COUNTER THIS. THEY NEED EXPRESS TO BE BANGING, AND WHEN I LAST TESTED, IT WASN’T. SO I’M REALLY NOT SURE OTHER THAN YOU TAKE THE BIRD IN THE HAND WITH 20B REV INSTEAD OF THE BIRD IN THE BUSH WITH 4B BUT GROWING TOPLINE MORE.

Hole 7: Your revenue growth math doesn’t account for the pricing lever running dry.

Adobe has been raising prices steadily. Creative Cloud went from $50/month to $60/month. They just introduced “Pro” tiers at higher price points. A meaningful chunk of that 10-11% revenue growth is price, not volume. At some point — especially with cheaper AI alternatives emerging — the pricing lever snaps. If you strip out price increases, organic unit/seat growth might be mid-single digits. That’s a very different business than the one you’re modeling.

I THINK ADOBE NEEDS TO SHIFT TO A USAGE BASED PRICING MODEL. THAT IS CLEARLY THE MODEL OF THE NEXT GENERATION.

FIREFLY WILL CANNIBALIZE THE BIZ. THAT’S WHAT IS NECESSARY. THAT IS THE BET.

THE EVIDENCE IT’S HAPPENING:

1. Credit consumption is exploding. Credit consumption grew over 45% quarter over quarter in Q1 2026. Adobe In Q4 FY2025, credit consumption increased 3x quarter over quarter. Adobe So back-to-back quarters of massive acceleration.

2. Higher-value usage is skewing up. Video generative actions grew more than 8x year over year and audio generative actions doubled year over year. Adobe These are premium credit actions — they burn more credits per use, which drives the consumption-to-upgrade flywheel.

3. The pricing architecture already exists. Firefly Standard is $9.99/month (2,000 credits), Pro is $19.99/month (4,000 credits), Premium is $199.99/month (50,000 credits). Saas CRM Review They’ve built a tiered credit system that’s genuinely usage-based. The more you generate, the more you pay.

4. Enterprise is on credits too. 1,770+ enterprise customers are already entitled to use AI agents through a new credit-based pricing model. MarTech And as subscribers consume more generative credits, they have the choice of moving to higher-value Creative Cloud offerings or acquiring Firefly Credit Add-ons. Adobe

5. Management is explicitly framing the growth algorithm around consumption. The strategy is “drive MAU, drive credit consumption, drive enterprise usage.” The Globe and Mail As usage increases, higher-resolution and denser outputs consume more credits, nudging users toward premium tiers and add-ons. This usage-to-upgrade pattern provides a durable path to ARPU expansion. Futurum Group

6. They’re embedding into LLM surfaces as consumption endpoints. They’re atomizing Photoshop, Express, and Acrobat capabilities as MCP endpoints, providing imaging, video, and productivity functionality in ChatGPT, Copilot and other conversational platforms. Adobe That’s pure consumption-based — every API call from ChatGPT burns credits.

—

Hole 8: You rate this a 7 confidence but you’re allocating 0.4%.

Your allocation tells me your actual confidence is lower than your stated confidence. A 7/10 confidence on a stock at a “decade-best opportunity window” with 50%+ margin of safety should command way more than 0.4%. The fact that you won’t put more in means your gut is telling you something your spreadsheet isn’t. Listen to your gut. Either this is the conviction buy you think it is and you should be at 2-3%, or it’s the speculative watch-and-wait that your allocation implies — in which case, why not just wait for the CEO announcement and June earnings before committing any capital?

I’VE INVESTED 1% ON INITIAL BET. I’M GOING TO TRY TO GET IT TO 1.5%. I’M SCARED, BUT I FEEL THIS IS THE RIGHT THING TO DO. KEEP IT BELOW 2%, BE OKAY WITH A 20% DECLINE WHICH TAKES 1.5 TO 1.2.

Hole 9: You haven’t modeled the actual bear case.

Your bear case is vague: “AI absolutely destroys design.” But what does that actually look like in the financials? Model it. What if net new ARR additions decelerate from 11% to 5% over 2 years? What if churn ticks up from ~8% to 12%? What if the pricing power evaporates and ARPU goes flat? At 5% revenue growth with 25% NI margins and a 12 PE, you’re looking at a $75B market cap — another 20% downside from here. Is your 0.4% position sized for that? Because “AI destroys design” isn’t binary. The slow erosion scenario — death by a thousand cuts over 5 years — is actually the more likely bear case, and it’s much harder to detect in time to sell.

THIS IS BINARY. THE BEAR CASE IS THE BEAR CASE, IT’S BAD. WE LOSE 20-40% OF OUR 1.5% INVESTMENT, BUT STILL MAINTAIN FUND HEALTH. IT’S A BET.

Hole 10: The one you should be most scared of.

You wrote: “this fundamentally rests on the bet against trend (AI job displacement).” Then you immediately reassure yourself that you don’t buy it. But you don’t have edge on this question. Nobody does. You’re making a macro call about AI’s impact on professional creative work — one of the hardest predictions in technology right now — and treating it as a given in your thesis. If you’re wrong about this single assumption, everything else is noise. Your moat analysis, your FCF math, your CEO speculation — none of it matters if AI makes a $20/month tool that replaces 60% of what Photoshop does for 80% of users. And you can’t put a probability on that. You said so yourself: “I definitely don’t know all I could.”

I’M NOT SAYING I’M RIGHT. I’M SAYING THE EDGE RESULTS FROM THE VALUATION. PEOPLE ARE CONFIDENTLY SAYING ADOBE IS LEFT FOR DEAD AT THIS 15 PE PRICE. IT’S LOWER PE THAN DAVE, THAN ADP, ETC.. YET IT’S A STRONG BIZ. WITH REAL POTENTIAL IN AI, AND SMART PRICING TO MATCH THE FUTURE. I COULD BE WRONG, BUT SO COULD THE CROWD, ALL I KNOW IS IF THEY’RE RIGHT THEY WON’T MAKE MONEY, IF WE’RE RIGHT, WE WILL.

The bottom line question I’d ask you: if this exact business — same revenue, same margins, same growth — were a private company you’d never heard of, and someone offered to sell you 0.4% for $5,600, would you buy it? Or would you say “interesting, let me see who the CEO is first, let me see if AI is actually a threat, and let me come back in 6 months”?

Because that’s what your allocation is telling me you actually believe.

Simple version: if Adobe liquidated tomorrow and sold everything you can physically touch or collect — cash, buildings, receivables, equipment — and paid off all its debts, shareholders would get nothing. They’d actually owe money.

Here’s the math:

Adobe’s total equity (assets minus liabilities) on the balance sheet is already thin — somewhere around $10-11B. But $12.8B of those assets is goodwill — the premium they overpaid on acquisitions like Marketo, Macromedia, Omniture, etc. Another ~$800M is other intangible assets (patents, customer relationships, acquired technology).

So:

Total equity: ~$10B Minus goodwill: -$12.8B Minus other intangibles: -$0.8B Tangible equity: roughly negative $3-4B

That means every dollar of Adobe’s “equity” — and then some — exists only because accountants say the brands and customer relationships they bought years ago are still worth what they paid. If those acquisitions turn out to be worth less than what’s on the books (goodwill impairment), equity evaporates further.

Why this matters practically:

It doesn’t kill a healthy company. Microsoft, Oracle, and plenty of great businesses have run with negative tangible equity. As long as cash flow keeps flowing, nobody cares. The subscription revenue covers everything.

But it matters in a stress scenario. If Adobe ever hits a rough patch — revenue declines, AI actually bites, a recession hits enterprise spending — they have no tangible cushion. No asset base to borrow against. No rainy day fund. They can’t sell goodwill to raise cash. Compare that to a company like Apple sitting on $160B+ in cash and investments. Adobe burned its cushion on $32B of buybacks at $350-500/share. That’s the damage you’re inheriting.

It also matters for exactly the take-private scenario we discussed. A PE buyer looking at Adobe sees negative tangible equity and thinks: “the only thing backing this valuation is future cash flow.” Which is fine if you believe in the cash flow — and at $8-10B/year it’s very real — but it means there’s zero margin for error. If cash flow stumbles, there’s no asset floor under you.

In your own words from the memo: they spent $21.5B in two years on buybacks at $400+ and the stock is now $244. That’s not just bad timing — it’s the reason tangible equity went negative. They literally bought back more stock than the company’s tangible net worth. The previous CEO got paid $51M while doing it.

AI’S REBUTTLE TO MY REBUTTLES:

Your rebuttals are solid. Let me grade them honestly.

Hole 8 rebuttal: Moving from 0.4% to 1.5%. Good. That’s a real position now. And your risk framing is right — a 20% drawdown on 1.5% takes you to 1.2% of the portfolio. That’s survivable. You won’t panic-sell. You won’t lose sleep. And it’s big enough that if you’re right and this re-rates to a 20-25 PE over 2-3 years, you actually make meaningful money. 1.5% is the right size for a high-conviction contrarian bet with known unknowns. I have nothing to push back on here.

Hole 9 rebuttal: “It’s binary, it’s a bet.” I respect the intellectual honesty more than I respect the modeling. You’re saying “I know I can lose 20-40% of 1.5%, and I’m okay with that.” Fine. That’s a $8,400-$16,800 max loss on a ~$560K portfolio. You’ll survive. But I’d push you on one thing — it’s NOT actually binary. The slow erosion scenario is the one that traps you. Binary is easy — you either win big or cut the loss. The scenario where Adobe grows revenue 6% instead of 10%, PE stays at 14, stock goes sideways for 3 years, and you sit there watching your opportunity cost pile up while other positions compound — that’s the painful one. Know your time horizon. If this hasn’t started working in 18 months, revisit ruthlessly. Don’t let “the thesis hasn’t been disproven” turn into “I’m married to this position.”

Hole 10 rebuttal: “The edge is in the valuation, not the prediction.” This is actually the strongest thing you’ve said in the entire memo, and you should have led with it. You’re not saying “AI won’t disrupt design.” You’re saying “at 15 PE and 10x FCF, enough of the disruption risk is already priced in that I have asymmetric upside.” That’s a fundamentally different claim, and it’s a much better one.

You’re right — if the crowd is correct that Adobe is dying, they don’t make money from here because it’s already priced for decline. If the crowd is wrong and Adobe navigates AI successfully, you make 50-100%+ on a re-rate. That’s the asymmetry. Heads you win big, tails you lose a little. That’s exactly the kind of bet you should be making at 1.5% of portfolio.

The comparison to ADP is sharp. ADP trades at 30+ PE. Adobe trades at 15 PE with similar margins, similar recurring revenue quality, and faster growth. Is Adobe’s business really half as valuable as a payroll processor? The market is saying yes. You’re saying no. One of you is wrong, and at 1.5% you’re getting paid handsomely if it’s the market.

My final honest take on your position:

You’ve done the work. You know the risks. Your sizing is disciplined. Your thesis is clear — valuation asymmetry, not a prediction about AI. The usage-based pricing evidence gives you a real catalyst beyond just “new CEO.” The small business formation wave gives you a secular tailwind nobody’s modeling.

The three things I’d write on a sticky note and put on your monitor:

1. June earnings — watch BPC segment growth and any disclosure on credit revenue as a percentage of total ARR. That’s your thesis validator.

2. CEO announcement — Wadhwani is fine, Whitehurst is a catalyst, a bad pick or a 12-month drag is your exit trigger.

3. 18-month clock starts now. If the stock is still at $240-250 in October 2027 with no re-rate despite continued revenue growth, you were wrong about the valuation gap and need to move on.

The bet is good. The size is right. Now be patient and don’t touch it until one of those three things happens.

~Don

https://x.com/donversationz

Www.LinkedIn.com/in/donstein

www.MEETDONSTEIN.com