You would all fall asleep reading about legislation… 💤💤💤..so I made a video for us instead!

We all love AI…. but this week, it’s slightly uglier cousin, Crypto, is making noise! You’ve heard the term ‘bit-coiners’ and now the new word is ‘suite-coiners.’ Referencing this new wave of crypto coming from Wall Street (industries who traditionally wear suits).

“Hey! Welcome to my blog, Don’s Daily!”

Hey, I’m Don! I’ve been building career memories for a decade. Over the last three years I’ve been reinvesting my own capital and time back it into my business. All the while learning and growing my net worth via public markets and crypto.

Over that same period, I also hosted 50+ virtual events with some of the world’s best VC investors and founders for our CEO group. Prior to all that, aside from my first job at Meta, I was lucky enough to raise $10 million in my twenties; doing my best to learn business, investor relations, and the startup mindset all at the same time. Maybe some of you can relate.

All that’s to say, I love business, I love money, I love to try and leverage my time.

This year, I set the goal to publish a thoughtful blog every Monday.. 52 of them! Don’ Daily is a recap of the entrepreneurship adventures I collect, as well as the new lessons I’m constantly learning from doing. My hope is that this entertains, inspires, and influences new creative ideas for you. Every Monday.

If you need anything at all, or if you want to work together, lmk!

There are three Crypto bills that matter; Genius, Clarity, and RFIA

Setting the stage in the most simple terms

Genius Bill already passed into law during the Summer.

Clarity Act was passed in the House, but stalled in Senate.

RFIA is the third separate bill, which aims to settle the differences Senators are fighting over within Clarity.

RFIA is specifically focused on making it clear how CFTC and SEC play nice together. One way they’re doing this, is with the invention of “ancillary assets.”

Explanation of “Ancillary Assets”

These assets are distinguished because they do not grant the holder traditional equity-like rights, such as ownership stakes, dividends, profit-sharing, or voting rights in a company or project.

Instead, they provide rights utility, access to a network, or other non-financial benefits tied to a blockchain protocol.

They are “ancillary” because they support or are incidental to a broader investment but aren’t core securities. Under RFIA’s framework, these assets start under SEC oversight to ensure initial investor protections (e.g., disclosures during fundraising). But they can transition to Commodity Futures Trading Commission (CFTC) jurisdiction through a self-certification process if the project decentralizes—meaning no single entity controls the network, reducing risks of manipulation or fraud.

Examples could include certain utility tokens in decentralized projects, like those used for governance in a DAO (Decentralized Autonomous Organization) without direct financial claims, or tokens for accessing decentralized apps.

This concept helps bridge the gap between securities (SEC-regulated) and commodities (CFTC-regulated), allowing projects to evolve without permanent SEC burdens if they meet decentralization criteria. It’s a compromise to foster innovation, as overly broad SEC classification has historically stifled crypto development.

RFIA proposes scaling regulatory requirements based on the size and impact of a digital asset project, rather than applying blanket rules to all. I.e. If a project raises more than $5 million in value through token sales or has trading volume exceeding $5 million annually.

Smaller thresholds might apply for ongoing reporting, like $1 million for basic originator info. This offers flexibility for smaller projects. Startups or experimental tokens below these thresholds face minimal red tape, encouraging grassroots innovation without costly compliance (e.g., no need for full SEC-style prospectuses for a small NFT collection). Requirements ramp up as the asset grows—e.g., semiannual reports for mid-sized assets, full audits for high-volume ones

Differences Between RFIA and CLARITY Act

RFIA didn’t “suddenly” appear—it’s an evolution of prior legislation—but its late 2025 push coincides with CLARITY’s Senate delays, positioning it as a Senate-driven complement. They are complimentary, to be very clear.

Clarity Act is essentially a CFTC empowerment bill to reduce SEC overreach. Focused on “market structure” for digital commodities (e.g., tokens on mature blockchains). It emphasizes shifting oversight to the CFTC for decentralized assets, exempting them from SEC rules if the blockchain is “mature” (no centralized control) and sales are under certain limits. It covers exchanges, brokers, dealers, anti-money laundering (AML) under Bank Secrecy Act, and provisional registrations.

RFIA creates a “clear line” between securities (SEC) and commodities (CFTC), with transitional paths for assets to shift regulators, plus joint rulemaking to minimize agency conflicts. RFIA is broader and more comprehensive, covering not just market structure but also tax treatment, consumer protections, banking integration (e.g., allowing banks to custody, stake, and process payments for digital assets), stablecoins, smart contracts, and illicit finance. It introduces concepts like “ancillary assets” and hybrid SEC-CFTC jurisdiction, with tools like regulatory sandboxes for testing. RFIA also modernizes banking laws to integrate crypto safely, which CLARITY touches less on.

There’s many nuances - RFIA excludes tokenized securities from its digital asset definitions and ties rules to thresholds (as above), making it more flexible. CLARITY uses blockchain maturity tests and semiannual disclosures, which some view as rigid - but if you take a Birds Eye approach, they are both here to usher in an era of digital property/asset innovation.

Why RFIA Emerged During CLARITY’s Stall

Introduced May 29, 2025, by Rep. French Hill (R-AR). It advanced through House committees (Financial Services and Agriculture) with bipartisan support, passing the House in July 2025 (per prior context; results confirm passage and Senate referral on Sept 18, 2025). However, it’s stalled in the Senate Banking, Housing, and Urban Affairs Committee due to:

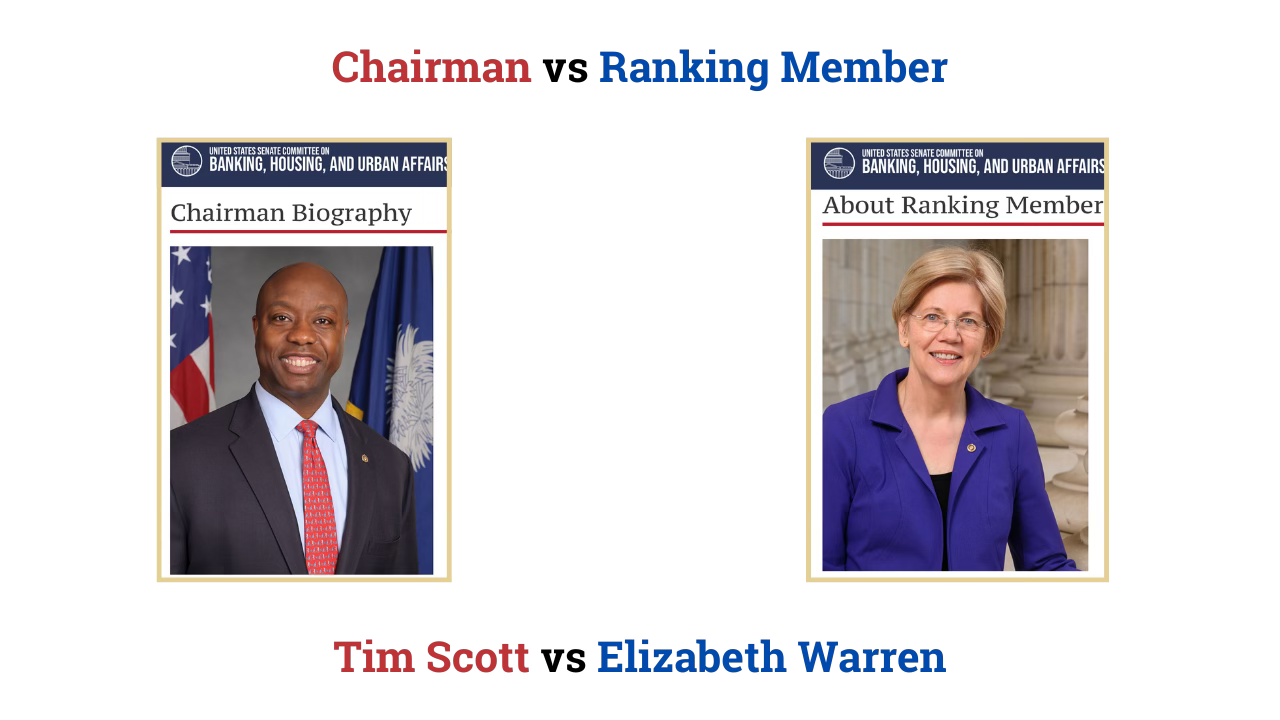

Specifically, Clarity has two leaders at odds within the Senate Banking Committee. Chairman Tim Scott vs Ranking Member Elizabeth Warren. Chairman has more power, but Elizabeth has more pull.

RFIA thankfully does seem to blur the lines a bit more — being led by Cynthia Lummis (R-WY) and Kirsten Gillibrand (D-NY). Go ladies go!!! We are cheering for you. A 182-page RFIA discussion draft was released by the Senate Banking Committee on Sept 5, 2025, shortly after CLARITY’s House passage. Lummis began tweeting about the “RFIA of 2026” in late December 2025, framing it as reinforcing CLARITY by distinguishing securities/commodities.

RIFA does not make Clarity less important, or smaller

Lummis explicitly says RFIA “will reinforce the Clarity Act” in distinguishing assets, suggesting it builds on CLARITY rather than replacing it. RFIA could serve as the Senate companion bill, leading to a conference committee to merge them into a final law.

RFIA expands the framework. CLARITY might get “stripped out” or amended in reconciliation (e.g., adding RFIA’s banking provisions or thresholds), but this strengthens rather than diminishes it. CLARITY isn’t being gutted to pass; instead, delays stem from Senate negotiations, and RFIA offers compromises (e.g., more SEC input) to break the logjam.

Not to mention, RFIA is earlier-stage than CLARITY (since it already passed the House and awaits Senate action). RFIA doesn’t even have a bill number assigned yet (prior was S.2281 in 118th).

Let’s use $AAVE token as an example

Let’s use the $AAVE token as an example, created by AAVE Labs. $AAVE is the native governance token of the Aave protocol, a fully decentralized, non-custodial lending/borrowing platform. It’s recently been under fire by it’s token holders because Labs is debating who owns the IP right to brand.

Currently, $AAVE provides voting on protocol upgrades, staking in the Safety Module, and utility access, but no direct “equity” in Aave Labs or enforced profit-sharing. Some holders want more value accruing directly to the token/DAO, but this is an internal governance issue, not a regulatory one. RFIA-style clarity doesn’t exacerbate it—instead, it protects the decentralized protocol (and thus token utility) from heavy SEC oversight, while Labs remains a service provider (not the “owner” of the token’s value).

Aave is already highly decentralized (governance handed over in 2020, no admin keys held by Labs), so AAVE would likely qualify for commodity status with minimal ongoing burdens. The SEC closed its 4-year investigation into Aave in December 2025 with no enforcement action, explicitly avoiding classifying AAVE or protocol operations as unregistered securities. Under RFIA’s ancillary assets category such tokens are presumed not to be securities (shifting to CFTC/commodity oversight if decentralized).

In short, regulation like RFIA makes decentralized utility/governance tokens safer and more valuable by confirming they’re not securities.

Leading crypto projects will benefit big, but Jan 15th matters a lot

CLARITY already passed the House on July 17, 2025, and was referred to the Senate, where it’s stalled without a vote. The Senate would need to pass its own version (likely based on the RFIA draft or a merged text using CLARITY as the base) before the two chambers reconcile differences in a conference committee.

A markup (committee debate and vote) for a Senate crypto bill was eyed for mid-December 2025 by Senate Banking Chair Tim Scott, but Democrats pushed back with a counteroffer, leading to delays into early 2026.

Any final bill requires Senate passage first (or a merged version). Negotiations are centered on the Senate’s drafts, with a markup now slated for January 15th, 2026 (rumors).

Clarity Drives Inflows and Formation: By shifting oversight of decentralized assets to the CFTC (with clear “maturity” tests and exemptions for DeFi developers/transaction verifiers), it creates predictable rules that encourage offshore projects to relocate to the U.S. and new founders to launch here. Industry experts note this could lead to a “wave of adoption” for compliant chains, with startups flocking to build on platforms classified as commodities.

RFIA helps VC-funded startups scale operations, attract institutional capital, and integrate with traditional finance without fearing SEC enforcement actions. For example, startups building DeFi or tokenized assets can use sandboxes to prototype without full registration, reducing legal costs that often eat into early-stage funding. If these both get enacted, Clarity first, then RFIA, we are (hopefully) booming!

Not financial advice.

P.S. Special shout out to the bipartisan pro-crypto Senators who are working hard with Cynthia and Tim to make this happen: John Kennedy (R-LA), Katie Britt (R-AL), Thom Tillis (R-NC), Catherine Cortez Masto (D-NV), Bill Hagerty (R-TN), Bernie Moreno (R-OH), Ruben Gallego (D-AZ), Mark Warner (D-VA), Kirsten Gillibrand (D-NY), Angela Alsobrooks (D-MD), and John Hickenlooper (D-CO).

If you made it this far, you are a hero!

Here’s how I can help you with your early customer acquisition:

I’m looking to select 1 AI startup and do a breakdown of their product to our readers! Please submit your product here for demo if interested!! Can’t wait to see what you all have been cooking.