[Week 5/52]: Amazon creates a Mona Lisa (almost) every day, and is on track to become the first company in history to hit $1 Trillion of annual revenue

When you put the numbers, robots, and team into perspective... Amazon operations are one of the most beautiful pieces of creation in human history. Mona Lisa ~$850 Million.. vs Amazon ~$2.6 Trillion.

[Preview]

Here’s the Amazon investment thesis I’m working on for myself. I already own a stake in the company, and am doing deep-dive research to figure out if I want to increase my position. This is for self-educational purposes only, do your own research, validate any estimations, and do your own due diligence (DYODD).

I believe Amazon (AMZN 0.00%↑) is on track to become the first company in history to hit $1 Trillion of revenue per year. If my projections are correct, this happens between 2029-2032’ish. Crazy. The other Mag 7s are projected to be at roughly half a trillion of revenue at that same time in the future.

[Thought Exercise]

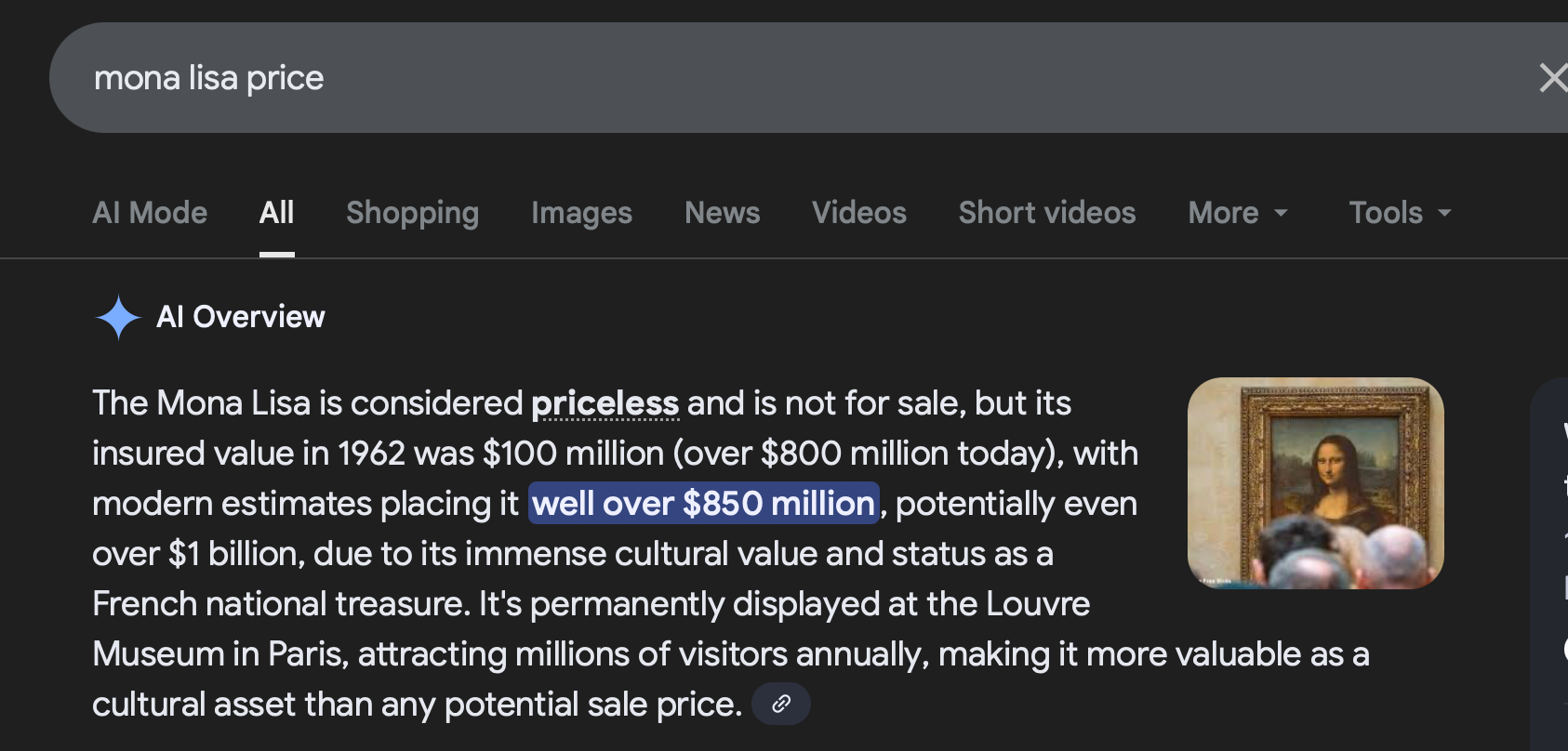

I had to look up the Mona Lisa’s valuation. I thought it would be around $150 Million. But I was incorrect, and far off. As back in the 1960’s the insurance value was already surpassing $100M.

Today, the Mona Lisa is valued at around $800M (insurance value). For the sake of argument, let’s assume each year the Mona Lisa generates about $4 Billion of indirect revenue to the Louvre Museum. This single painting is so highly coveted that French President Emmanuel Macron announced a $800M+ renovation project (2025) to renovate the Louvre and give Mona Lisa her own private room. She deserves it because the Louvre Museum sells about $200 Million of tickets per year, and pretty much every guest arrives excited to see the Mona Lisa. On top, it’s estimated she brings an additional $3 Billion through tourism each year.

Amazon makes that same $4 billion every two days... Amazon creates almost 200 Mona Lisa’s every single year ($700 billion in revenue). And, Amazon generates in revenue the value of the entire Louvre every single week (~$10B).

Amazon’s 2025 TTM revenue is about $700 billion, or roughly $2 billion per day. So maybe it’s not quite making a Mona Lisa every single day, but at their current pace of revenue growth… Amazon will be be recreating the value of the Louvre every single day between the years of 2029 and 2034, and that’s assuming their growth rate slows ( Revenue grows 10% stabilized after the pandemic craze of 20-30% annualized growth, hitting goal of $1 Trillion of revenue per year).

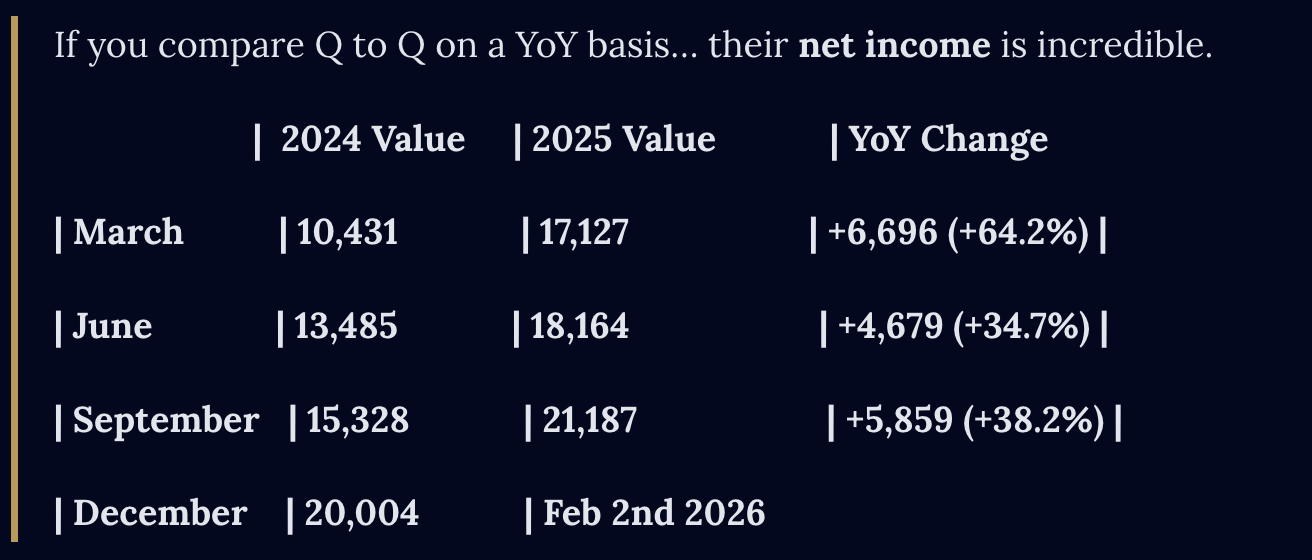

If you compare Net Income from the equivalent 2024 quarter to their 2025 quarter, you could easily argue they are growing profitably even faster than revenue as their vertical integration efficiencies in logistics, robotics, AI, grocers, AWS, and package delivery kick in. This is a great American company.

Looking at the numbers like this, you’ve got to assume Amazon delivers 26+ billion of net income for Q4. Bringing the annual total to $80.. and putting 2026 on track to most likely be their first year of $100,000,000,000 in profit. I wrote that out for effect.

Let me restate, they are currently on track to generate $100 Billion of profit within the next year, and this lines up to Justin Post, an analyst at Bank of America Securities, estimates hovering around $800 billion in revenue (+12% YoY). That’s a milestone, I’ll say. That puts them in the category with Nvidia, Apple, MSFT, Google, Saudi Aramco.

But here’s where it gets interesting…

Amazon will the the first of any company in human history to hit $1 Trillion of revenue per year.

Google would be doing roughly half that at their current growth rate, even Apple would only be doing about $600 billion of revenue at the time when Amazon surpasses $1 Trillion. Saudi Aramco also about half of Amazon, and Microsoft about $400 billion per year at that projected date.

For the record, Walmart also matches Amazon’s current revenue rate of $600-700B per year, but growing at a much slower rate, and would likely get out paced by Apple by the time a second company hits $1 Trillion in annual revenue.

In Summary.

Amazon should likely become the first company in the world to hit $1 Trillion of Revenue

Amazon manufactures the value of a Mona Lisa every couple days in 2026

Amazon recreates the Louvre every single week in market value

IF Amzn grows 30% YoY in Q4, which is a fair estimate because it would match what it did in Q1-3, then it ends 2025 with about $80 billion of net income. If it then grew 30% again next year… we’re looking at $100 Billion of Net income. Meaning if it holds its current Price-to-Earnings Ratio at 33 P/E, we should see it grow from ~2.5 Trillion to ~3.3 Trillion in 2026.

Said in a less professional way → Amazon’s Net Income is Bonkers.

Amazon did $59 billion of Net income in 2024… and in only 75% of the time it’s already hit those numbers in 2025. Amaon reported $56 Billion in the first 3 quarters. So basically whatever Amazon reports in Q4 is pure growth above last years FY numbers. Insane.

Not to mention their Balance Sheet.

Amazon has almost a Trillion dollars worth of assets.

$700B to be exact, and doubling every ~5 years.

In my view, the even more impressive milestone is they’re closing in on $500 Billion of Shareholder Equity. SE is their assets minus liabilities.

I think of Shareholder Equity as all the retained return on their investment over the decades. Current TTM ROE stands at 23.62%, meaning they’re growing equity value roughly 23% per year.

All of those above paragraphs are to say…. their numbers are good. Really good.

So now, you should next be asking yourself, what trends/products are growing the most for Amazon?

This is when the numbers become tangible, and you become even more impressed with what humanity is capable of building with enough time and resources.

“Digit Robot” by Amazon

Look at these humanoid robots they have working the factories.. and this video is from 2023! Just imagine what they have now:

They have Humanoid robots, as well as traditional smart-robots that are stationary. Amazon has optimized everything.

These are my personal favorites of the non-humanoid style robots they use: they are the Hercules Robots they invented.

These Hercules robots motor around the warehouse, operating on a mix of computer vision and AI Robotic-Specific Foundation Models which Amazon custom built.

For example, they’ve created custom vision models trained specifically for warehouse scenes. And are even optimizing the hardware for light weight models that run on robots edge hardware. This means they can have faster reaction time as there won’t be the delay of sending everything to the cloud when processing AI.

The centralized brains behind all this though, is Deep Fleet AI, coordinating 100s of robots at once, avoiding traffic jams, collisions, etc.. Deep Fleet prioritizes power efficiency, and logistics of the robots within every warehouse.

If you care, here are a list of the video resources I used. It’s just cool to see how tangible robots are in 2026.

Amazon Herculeus (1:58, great video clip from there)

Amazon DIGIT Robot at 2:08 OMG)

Now all that leads to a pretty hefty R&D budget. It is HARD to maintain this company, it is expensive.

R&D expense hit $100 billion.

They spend $165 billion on SGA.

It’s hard to fault their R&D spend when you see the ROI reflected in margins, up and down the scorecard. I’d probably feel most comfortable seeing their R&D growing around $12B a year, but I don’t know the details of how they’re spending, and the according ROI. So my opinion here is just that, an opinion.

P.s. I find this equally as mind-blowing as the robots, all of the robots run on fully custom specialized embedded chips, often ARM based, specifically created by Amazon, for Amazon. So they even have a little bit of Nvidia in their DNA. This company is incredible.

AI Play

In my opinion, so far developed but never complete, Amazon Bedrock, and Amazon Nova AI are the centerpieces of the Amazon AI strategy. Mainly because they’re building these tools with a very specific purpose.. delivering tokens at the most efficient price.

Meaning Amazon’s Nova doesn’t say “hi Don!”, or, “good morning,” no, it just does the job. It gets the job done for ~50% the cost.

Meaning Amazon Bedrock orchestrates which of the leading AI models (GPT, Claude included) will do the task most efficiently, then automatically routes the prompt to that solution.

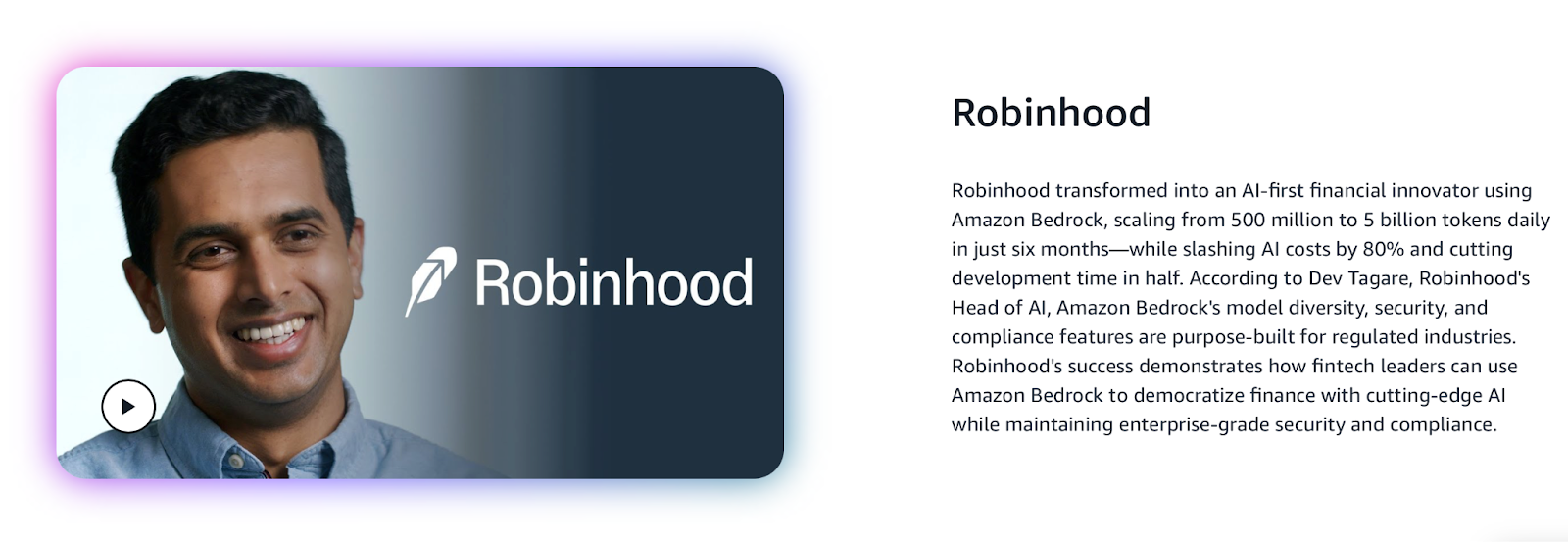

Companies like Robinhood seem to be happy, or at least happy enough to leave a testimonial regarding their experience on Amazon. This is the testimonial from Robinhood’s Head of AI, Dev Tagare.

I thought this quote from him was powerful, “AWS is our primary and really only partner for training, serving our inference of models.”

This makes sense because Robinhood is already built on AWS, and can easily build on top of their current data suite with Amazon’s AI tools. This is a massive Trojan Horse for the largest cloud provider in the world, shifting to AI cloud.

You can do a quick scan of the Nova family of models, they’e got it all! In house!

Nova Micro: Text-only model optimized for speed and low cost. Ideal for simple, high-volume tasks like quick text generation or basic queries.

Nova Lite: Multimodal (text, image, video inputs → text output). Fast and affordable for everyday tasks like content summarization or basic reasoning.

Nova Pro: Highly capable multimodal model balancing accuracy, speed, and cost. Suited for complex tasks like coding, analysis, or multi-step workflows

Nova Canvas for generating images

Nova Reel for video gen

Right now, some of the biggest and most impactful AI apps building on Bedrock come from major companies like Pinterest. Their new AI-powered discovery engine serves over 600M users worldwide with generative AI for personalized recommendations

Others killing it include:

DoorDash handles hundreds of thousands of customer support calls daily with their Bedrock-powered contact center solution, slashing escalations big time.

Adobe (boosting developer support accuracy)

NASDAQ (real-time analysis)

AstraZeneca (R&D drug insights with agents)

Vercel powers over seventy-five million AI-generated code suggestions for developers globally.

United Airlines (modernizing legacy systems for better customer experiences). Btw, I do think United has become wayyyyyy better as an airline. The service is now amazing b/c of the tech.

Amazon’s Bedrock AI has over one hundred thousand organizations on it, but these stand out as massive-scale ones. Here’s more customers if you want the resource.

Robinhood and others are going big on amazon. They moved high-volume tokens to Nova. Nova is looking like a GENIUS loss leader to lock in customers. Amazon bedrock gives you tools to build agents, and access to dozens of top models. Amazon Q is the software development platform. Coding, IDE plugins, enterprise search aka chat with your company data.

Bring it all together, you’ve got custom chips, robots, AI models…. and, groceries?

Yes that is right, the other part of my thesis is groceries.

InstaCart is a mess right now, and the only growing part of their business is selling ads. That’s not going to be sustainable for a company that is also going to be losing users to Amazon. They couldn’t expand to Europe, they have unhappy drivers, and just got caught up in a scandal where they were deceiving their customers. Big fine. Should be more IMHO as I’ve been paying for membership and getting ripped off by their scheme the whole time. Anyways, I digress.

Walmart and Costco, though incredible, also have this retail vs warehouse dilemma. At some point, it’s likely there’s enough pressure from Amazon Warehouses that Walmart will need to de-prioritize their retail stores in favor of same-day grocery delivery from distributed warehouses.

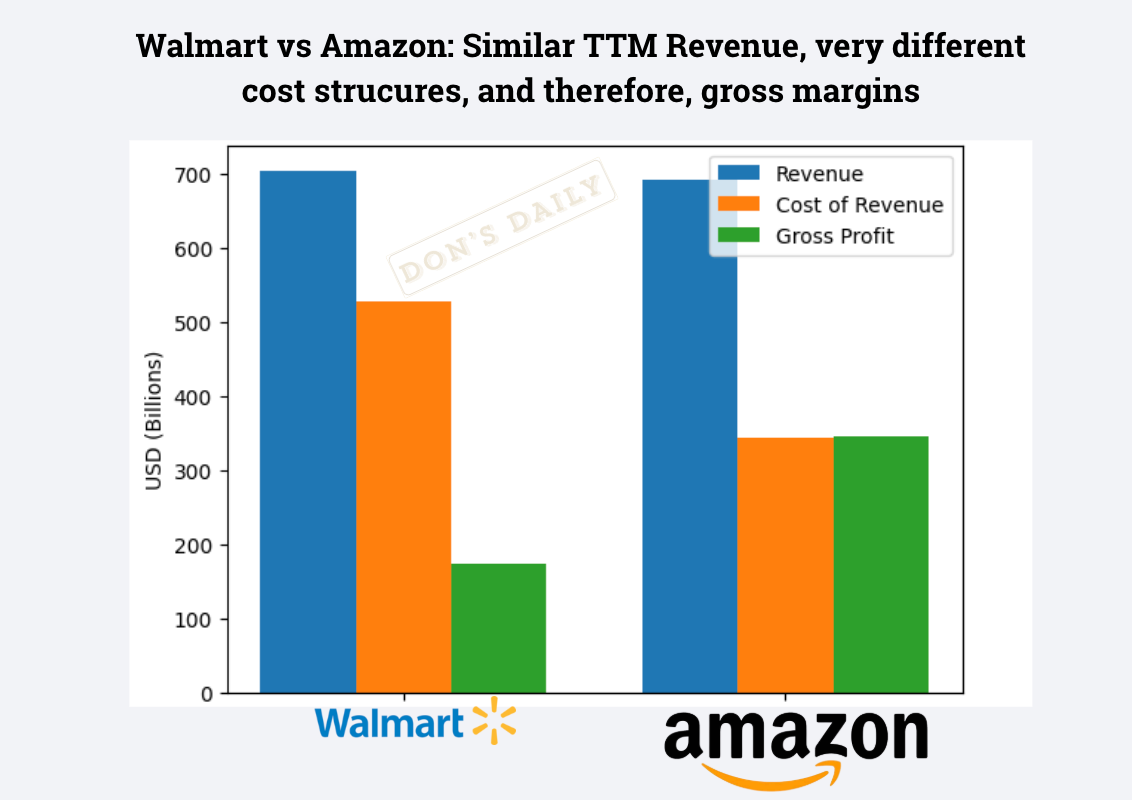

Groceries are going to be won by Amazon. Because Amazon is using groceries as a beachhead market to deliver EVERYTHING the same day, heck, eventually the same hour. They are skipping over the expensive Retail infrastructure, and investing in tech. This is most evident in the fact both companies generate about $650B, but Amazon has $300B+ of gross profits, and Walmart has $150B+. So Amazon is twice as efficient since Walmart is weighed down by Retail infrastructure fundamental to their business since 1962.

The divide in Amazon vs Walmart margins are most prevalent when looking at their trailing 12 months of Revenue and Gross:

Amazon is a dot-com baby, therefore this company is removing the retail experience completely, and instead making at home shopping just as convenient. This trend has be seen for years.. but what I’m saying is now that they have autonomy, they can take it to the next level; same day grocery, necessity, and product delivery.

With warehouse all over the world, autonomous driving opportunities in the future with Rivian, automated warehouses with Robots like Hercules and Digit.. it’s easy to see how produce will be delivered directly from a perfectly temperate controlled warehouse as opposed to an open grocery retail store with people walking around all day.

The prior is much less expensive to warehouse on a per/sf basis. This leads to lower prices for customers, and faster delivery times. As the bets Amazon has made unfold, and it eventually hits that $1 Trillion per year revenue mark in the upcoming 5 years. It’s going to be quite the sight to witness just how efficient they are at scale.

Leadership Team

I think a lot of people ask this question online, “Wait so is Jeff Bezos still at Amazon or not? I feel like he’s traveling all the time now.”

Jeff Bezos is still involved with Amazon as Executive Chairman.

It’s still his baby, he’s still running the show, the ship is still his. He’s just doing it in a way that lets him also travel.

He looks happy AF to me. I don’t understand why so many people hate on someone who worked so hard, built and incredible biz, and then got in great shape. Good on him. But, I digress!

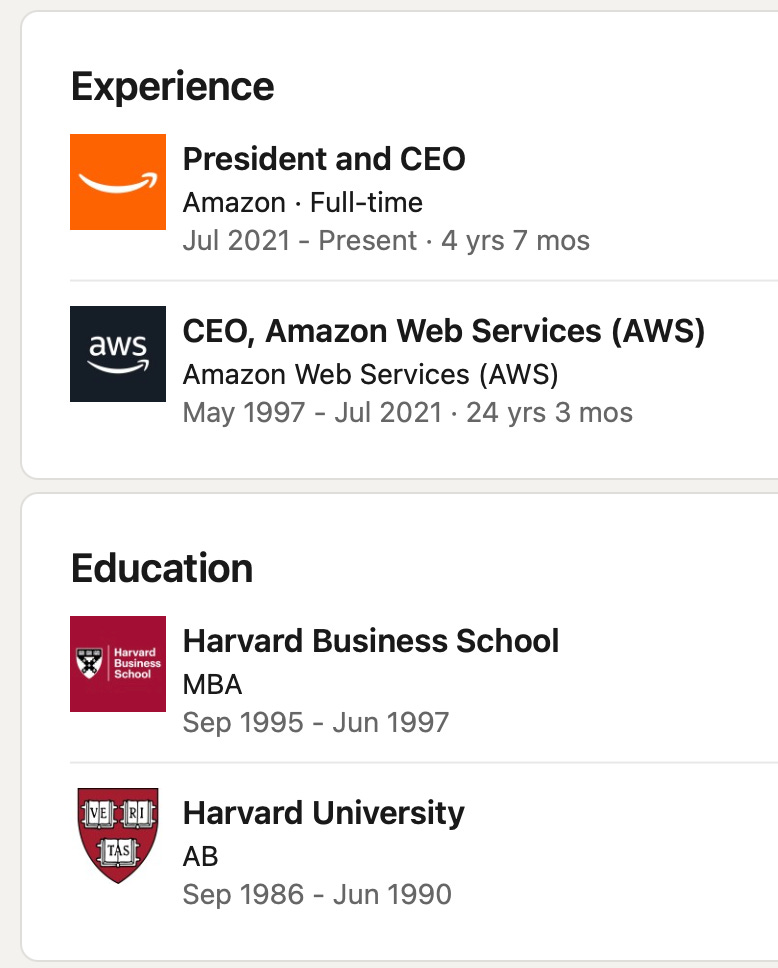

Who did Jeff hand over the CEO keys to?

Andy, of course.

He has one of the most simple resumes I’ve ever seen. From 1986 until 2026 he’s done two things; Harvard, Amazon 😂.

This guy is a rare breed. And a perfect fit for the Amazon ethos of efficiency.

Jassy has been there 25+ years, and so many of the leaders have been there with him the whole time. A close knit group I would presume.

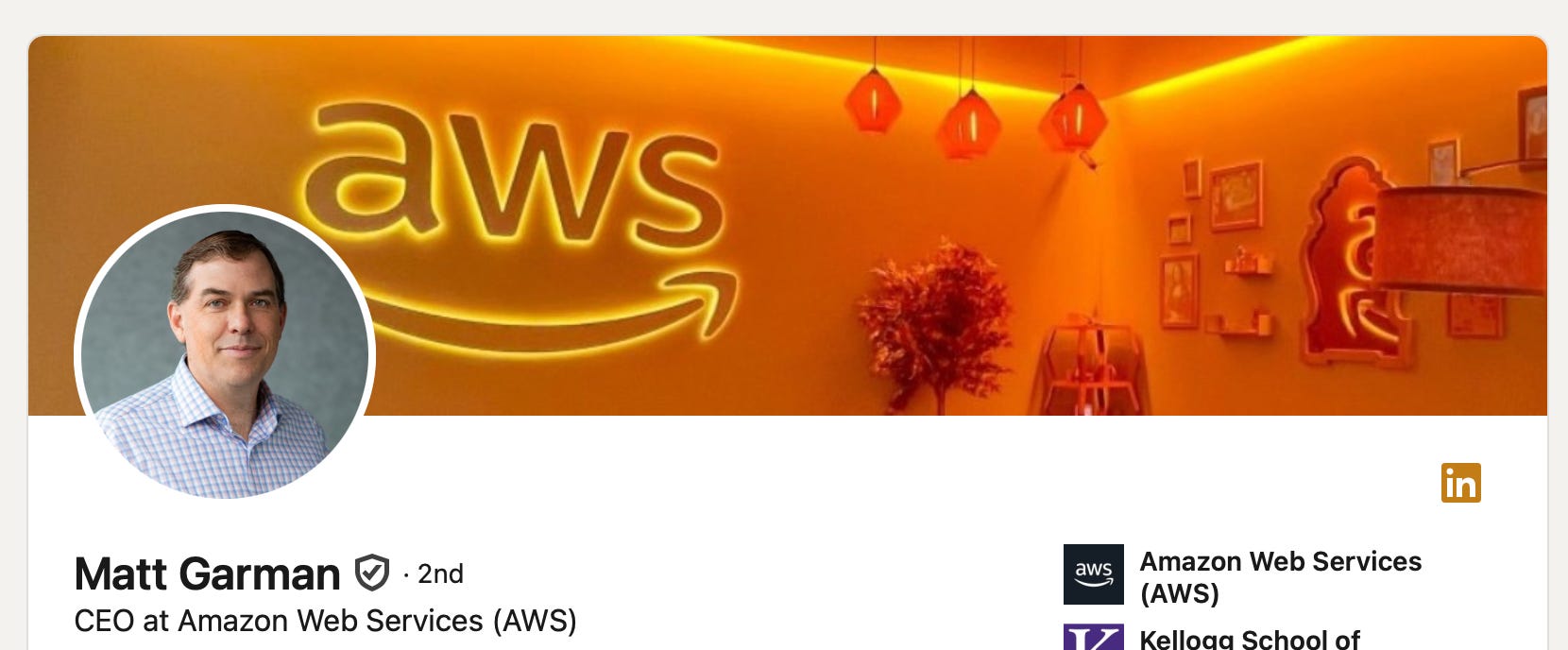

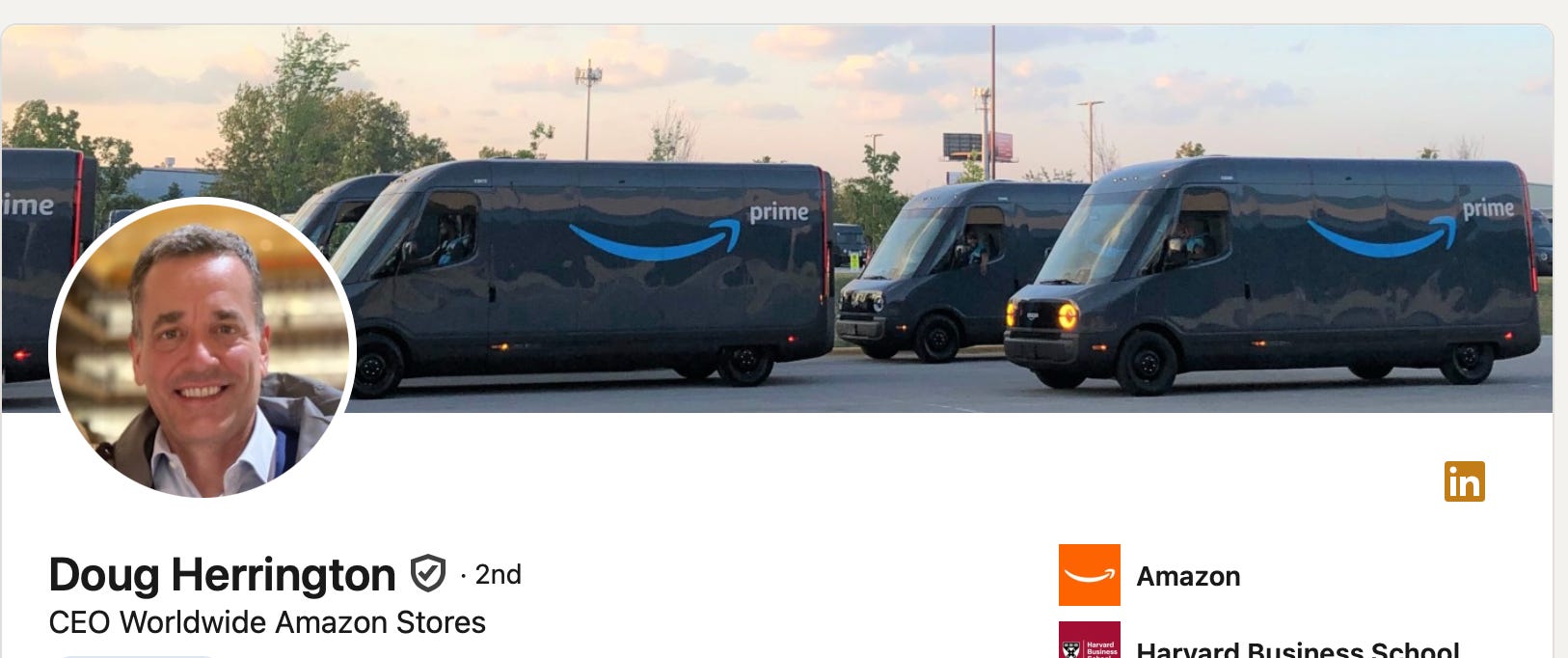

More teammates with 20+ years at Amazon

Matt Garman: Another key player to watch, is their Head of AWS. As you see, the battle for AI cloud is heating up. AWS is their advantage to take the leadership position in AI as well as Cloud. His Amazon tenure is 20 years.

Doug Herrington: And their CEO of Amazon Stores. The digital shopping experience we all know and love. FUN FACT, this guy was Head of Marketing for WebVan during dot-com bubble. Funny how the world works! His Amazon tenure is 21 years.

This is a dedicated team of smart people, who have worked together for decades.

What could derail the $1 Trillion Revenue goal?

CLOUD MARKET SHARE! Decreasing 1% a Q is bad. But it is relative, and a matters of context. Yes they might be losing %, but they're growing more than anyone else on an absolute basis.

Amazon has about 30% market share, Microsoft about 20%, then Google at 13%, and everyone else only holds 1-2%.

It’s fair to say that both Amazon and Microsoft clouds are growing 20 to 40% YoY, Amazon’s is growing slower, but Amazon’s has about a 50% larger base to begin with.

And so, assumingely what happens is like in five, ten years, they both equal market share, maybe even equal with Google. And, they’re probably doing like 50 billion bucks of revenue each. I guess what I’m saying, the pie is growing fast enough for everyone to feast for quite some time it would appear.

In ~5 years at these rates: AWS could be ~$250–350B → Azure parity, Google maybe slightly less.

Microsoft and Google are Trojan Horsing AI into a bigger cloud business. Where as, Amazon is Trojan Horsing AWS into a bigger AI business. The strategies aren’t quite the same because Amazon is starting from a much stronger position of leadership.

So yes, they lose market share on % basis, but the overall cloud infrastructure market is exploding right now, therefore their smaller share is of a larger TAM. I won’t complain about growing 20% on a $130B run rate.

AWS is adding more absolute dollars per year than anyone else, and should remain for the foreseeable future.

All three cloud companies are optimizing hard for the inference heavy future.

Latest from Synergy Research Group says cloud companies as a whole generated trailing 12 months revenue of around $390 billion. The entire full public cloud market growing is 20–22% in 2026, (IaaS, PaaS, hosted private cloud), but the infrastructure piece AWS dominates is the hottest part, Gartner analyst expect growth likely staying above 20% annualized for the next few years.

It’s a great market, growing fast, and Amazon is the undisputed leader in todays reality.

OK THE COMPANY IS INSANE! I’VE CONVINCED MYSELF. THE TECH, THE TEAM, ALL OF IT!

SO, what about the bottom line?

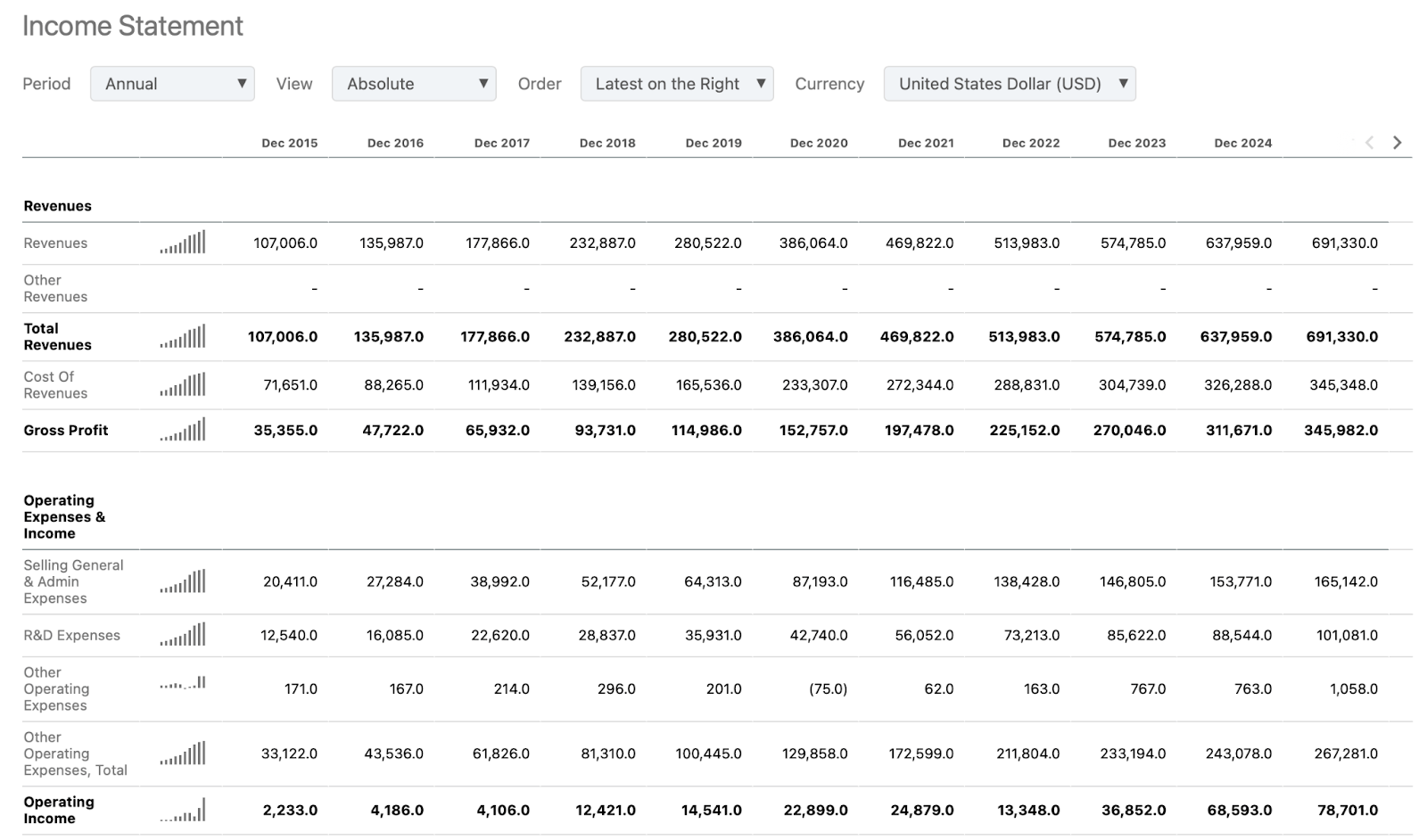

Here are the last 10 years of financials pulled from SeekingAlpha.

Incredible growth. In 2019 they had $280B of revenue, today it’s approaching $700B. This revenue is ripping, and, pushing a good amount of that to the bottom line.

For context, you can compare Amazon’s Net Income to Walmart’s below:

Walmart is sitting at about a ~45 P/E. Amazon sitting at about a ~33 P/E.

So amazon has higher market cap on an absolute basis, but relative to it’s net income, a much lower P/E multiple than Walmart. I prefer to bet on the tech giant, relative to the retail giant dressed up as tech. I’d say a fair price target for Amazon is $3.2 Trillion by EOY, this would assume about $80B net income and a 40 P/E, meaning their P/E would align more towards the premium Walmart is getting from investors.

Ending this with some quick technical analysis:

If I look at a 3 year trend, I would say it’s been trending up since 2023, within a pretty tight band. Stocks are inherently unpredictable, but it looks like a potential 220 pullback could happen, -10% decline, and that would be pretty normal within trend. I would love to acquire more if that’s the case.

DISCLAIMER – IMPORTANT – READ THIS

This post is for informational and educational purposes only and represents my personal opinions, research, and thought process as an individual investor. It is not investment advice, financial advice, a recommendation to buy, sell, or hold any security (including Amazon stock, ticker: AMZN), nor is it personalized to your financial situation, risk tolerance, or investment objectives.

I currently own shares of Amazon (AMZN) and may buy, sell, or otherwise transact in AMZN or related securities at any time, with or without notice. My personal positions create a conflict of interest, as positive commentary could benefit my holdings. I have no intention of updating this post if my position changes.

All statements about future performance, revenue projections (e.g., $1 Trillion annual revenue), profit estimates (e.g., $100 Billion net income), growth rates, valuations, price targets, or milestones are forward-looking and inherently uncertain. They are based on my assumptions, publicly available data, analyst estimates (such as from Bank of America), and historical trends — but actual results may differ materially due to market conditions, economic factors, competition, regulatory changes, company execution risks, or other unforeseen events. Past performance is not indicative of future results, and no guarantees or assurances are made.

Investing in stocks, including Amazon, involves significant risk, including the potential for total loss of principal. Markets are volatile, and you could lose money. Do your own independent research, consult a qualified financial advisor, tax professional, or other expert before making any investment decision, and verify all facts, numbers, and projections yourself.

This content does not constitute an offer to sell or a solicitation to buy any security. I am not a registered investment adviser, broker-dealer, or fiduciary under U.S. securities laws. Nothing in this post creates an adviser-client relationship.

Views expressed are mine alone and may change without notice. I am not compensated by Amazon or any third party for this commentary (beyond any general affiliate links or unrelated sponsorships, if applicable — none are present here).

By reading this post, you acknowledge and agree that you are relying on your own judgment and that I am not responsible for any investment decisions you make or losses you incur.

Do your own due diligence (DYODD). Invest at your own risk.